Al Ain

Al Ain

Known as the Garden City, Al Ain was once a vital oasis on the caravan route to Oman. Situated just 148 km east of the capital, Al Ain boasts several historical forts and archaeological sites. Fascinating insights into its origins can be found at the Al Ain Museum and the Natural History Museum at the University of Al Ain, both of which feature displays on life before the discovery of oil in the region.

The Hili Archaeological Garden has remnants of a Bronze Age settlement dating back to 2500 – 2000 BC. This site is the source of some of the richest archaeological finds in the area, several of which are believed to be more than 4,000 years old. The Jahili Fort, once home to the late ruler Sheikh Zayed bin Sultan Al Nahyan, is notable for its impressive main turret, which has four levels.

Al Ain is the most fertile region in the country, and its oasis supports a host of palm plantations and working farms. The city’s many parks are all beautifully kept and well worth a visit. Featuring play areas, benches under shady trees, meandering walkways and elaborate fountains, they offer tranquil hideaways for visitors and residents alike.

The Al Ain Zoo and Aquarium, spread over 400 hectares, is one of the largest in the Gulf region. It is home to a wide variety of species, both common and rare, and runs an ongoing breeding programme for endangered animals.

The city’s camel market is well known throughout the country and is the last of its kind. It provides the opportunity to see and hear traders discussing prices and listing the merits of their prized camels. The nearby animal souk is a similar experience, although it specialises in the sale of sheep, goats and other livestock.

Al Ain’s Old Prison affords the best views of the city and its surrounding oasis. It is a lone square turret in the centre of a gravel courtyard, surrounded by high walls. At night this historical building is illuminated, and offers a beautiful view when seen from the nearby camel market.

Overlooking the city is the majestic Jebel Hafeet, the highest mountain in the country. A road leads to the summit offering spectacular views in all directions. At its base are Ain Al Faydah natural spring and the Green Mubazzarah tourism resort.

Al Ain Roads & Streets

Al Ain Al Faydah – Hot Springs

Scenes at Al Wathba Camel Farm on way to Al Ain from Abu Dhabi

Jebel Hafeet Mountains – Al Ain

Reading Dubai’s road signs

Reading Dubai’s road signs

By Ashfaq Ahmed, Staff Reporter GULF NEWS

The expansion of Dubai warrants the need for a state-of-the-art, simple addressing system for the entire City.

The addressing system should be compatible not only to suit the needs of the residents but also assist visitors in locating address of various places. The system is in place in most areas of the city, but the people are not just using it.

The Dubai Roads and Transport Authority (RTA) has decided to enforce the comprehensive address system in city. The Authority wants residents to shift from landmark based address system to a real address system.

“The system will be enforced because the city is expanding and the landmark based address system will not work in future,” said Engineer Bader Al Siri, Director of the Traffic Department at the Dubai Roads and Transport Authority. Plans to deliver postal mails, parcels, telephone, and water and electricity bills are on the cards.

People dealing with any departments will have to give their full house or office address in future instead of just post box numbers.

Al Siri said the people should know where they live and where they work, including building number, road or street name and number, and the community number. “It is also essential in case of emergencies,” he said.

He said the address system is very easy but people need to change their mindset and should learn the system instead of relying on landmarks to tell their home or office addresses.

The project for the comprehensive address system, including building numbers, road and street names and numbers and the community numbers started in early 1980s. So far, some 69 per cent of the city area has been covered. Some 20 per cent more will be covered in 2006 and 2007 and some more areas in 2008. “It is an ongoing process as the city is expanding, new areas will be covered as they will be developed,” Al Siri said.

Gulf News conducted an indepth study on road signs in Dubai in order to explain to its readers what they stand for, what they mean and how to follow them.

To start with, every one should have the latest edition of the Dubai Tourist Map, which is easily available in shops. The map is particularly required before the start of a trip by an individual, who is not familiar with Dubai roads.

Dubai is currently divided into nine sectors and each sector is further subdivided into a number of communities. There are currently 129 communities in Dubai are expected to reach 150 in a few years time with the development of new areas.

Each community possess a unique three-digit number and name. The Dubai tourist map shows the general location of the community within Dubai. For Example, if the community number is 376, it means that the area is located in Sector 3 and the community number is 76.

All main routes in Dubai are numbered. Highways connecting other emirates or main cities in the UAE are designated as Emirates Route or E-Route. They carry their number within a falcon emblem and possess two or three digits.

Four E-Routes pass through Dubai. They are E 11, connecting Abu Dhabi with Sharjah and Other Northern Emirates, E 44, connecting Dubai with Hatta, E 66 connecting Dubai with Al Ain and E 77 connecting Jebel Ali with Lahbab. The E-routes are the land routes to neighbouring countries as well. For example, E 11 connects the UAE with Saudi Arabia and Oman while E 44 connects the UAE with Oman.

Main roads connecting areas within Dubai Emirates are designated as Dubai or D-Route. They carry a two- or three-digit number in a fort emblem.

D-Routes parallel to the coast are numbered evenly starting from D 94 and decreasing as one goes away from the coast whereas, D-Routes perpendicular to coast are numbered odd and increases as one moves away from Abu Dhabi to Sharjah.

Major roads surround a community and these roads usually possess a name and three-digit number.

Streets within a community possess two digits number (from 1 to 99) and these numbers are repeated in each community.

Buildings on each street are numbered sequentially. Except building numbers, all the information is available in the tourist map to assist drivers to plan his route prior to starting his journey.

Guide signs are placed on all approaches to an intersection and in advance of ramps and all the interchanges on numbered routes. Information containing in the guide signs is essential for the motorist during his journey. These signs help motorist to reach an area/community he is interested in.

Guide signs placed on approaches to intersections display the numbers of the intersecting routes, direction to be taken in order to reach to the intersecting routes and the name of the area or community where the route ends physically.

Each numbered route is associated with the destination that is the community name where the route ends physically along with a major intermediate destination. Motorist should know that guide signs placed on the roads will not display all the areas names through which the route passes.

In addition to the numbered routes, signs that provide assistance to motorist to facilities like hospital, parks, shopping centres, hotels, etc are called supplemental destination signs.

Special signs are placed on roads to guide motorists to these places. Information contained on these signs display the name of that facility along with their symbols and the direction to be taken in order to reach that facility.

Community maps are placed at the main entrance of the community and at locations where people can park and look at it. To help find your way every map has an arrow to show where you are currently located. It also shows other facilities located within that area like schools, parks, gas stations, mosques, parking lots and post offices.

Inside each community, each street is identified by a sign containing the street number and name. Street number signs are placed at all turnings into a community from the main road and all junctions within a community. Street number signs also contain community number.

A building number plate is placed near the main entrance of a building. Odd numbers are allocated for buildings on left of the street and even numbers are on the right.

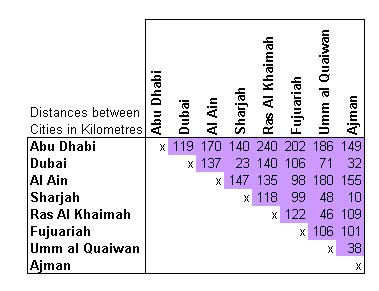

Distance between different Cities in UAE

All is not lost: 12 rules that can save you further losses

All is not lost: 12 rules that can save you further losses

With the markets sliding leaps and bounds, you need to keep your calm and find ways to cushion the free fall. In a book review of Zurich Axioms, our expert Kanu Doshi, talks about 12 strategies that can help you reduce your loss.

Reviewer’s Note:

The author (Max) son of a very wealthy Swiss citizen by name, Franz Heinrich, (whom Americans preferred to call Frank Henry), jotted down all the principles of speculation strategies, particularly in stocks, adopted by his father and his father’s several other Swiss friends to make large fortunes on the Wall Street in USA in roaring Eighties. Principles perfected by these Swiss gentlemen have therefore been called “Zurich Axioms” by Max.

Enumerated below are twelve major principles and sixteen minor ones with brief comments by Kanu Doshi on each of them:

First Major Axiom: On Risk

“Worry is not a sickness but sign of health. If you are not worried, you are not risking enough.”

Adventure is what makes life worth living. Every occupation has its aches and pains. The rich have to worry about their wealth. But, if there is a choice between remaining poor and worry-free, the selection is obvious. It is better to be wealthy and worried than to be worry-free and poor.

Minor Axiom I:

“Always play for Meaningful Stakes.”

If you invest Rs. 1000 and your investment doubles, you have only Rs. 2000 and are still poor! So if you want to be rich, you must increase your stakes.

Minor Axiom II:

“Resist the allure of diversification”.

Firstly, diversification negates the earlier principle of playing for meaningful stakes. Secondly, it may keep you where you began so that your gains on few will cancel out the losses on the other few. Thirdly, it entails keeping track of many more items leading to confusion and occasional panic.

Second Major Axiom: On Greed

“Always take your profit too soon.”

Lay investors having made the investment tend to stay too long on it out of greed for higher profits. But, one must conquer this weakness and book profits soon. If one is less greedy for more profits one will take in more. Don’t stretch your luck. In effect, it suggests, SELL sooner than later.

Minor Axiom III:

“Decide in advance what gain you want from the venture, and when you get it, get out. Decide where the finish line is before you start the race”.

This is self explanatory and hence needs no comment.

Third Major Axiom: On Hope

“When the ship starts to sink, don’t pray, jump”

This axiom is about what to do when things go wrong. Learn how to accept a loss. One should accept small losses to protect oneself from big ones. When the market starts falling, sell, take your money and run!

Minor Axiom IV:

“Accept small losses cheerfully as a fact of life.”

Expect to experience several smaller losses while awaiting a large gain.

Fourth Major Axiom: On Forecasts

“Human behavior cannot be predicted. Distrust anyone who claims to know the future, however dimly.”

The story of a monkey throwing darts on the stock exchange page of a newspaper, to select the companies to buy, and coming out a winner is too well known to be recited. Recent news from London, further proves the truth, when an untrained chemist’s stock selections, in a widely publicised contest open to all and sundry, registered higher appreciation over several full time highly qualified fund managers’ well researched selections. Human events cannot be predicted by any method by anyone and, hence, don’t trust anybody’s predictions.

Fifth Major Axiom: On Patterns

“Chaos is not dangerous until it begins to look orderly.”

The truth is that the world of money is a world of patternless disorder and utter chaos. This axiom is a commentary on Technical Analysis – a branch of investment strategies based on charts and patterns. The fact is, no formula that ignores own intuition’s dominant role can ever be trusted.

Minor Axiom V:

“Beware the Historian’s Trap”.

This is based on the age old but entirely unwarranted belief that history repeats itself.

Minor Axiom VI:

“Beware the Chartist’s Illusion”.

Life is never a straight line. Let us not be hypnotised by a line on a chart.

Minor Axiom VII:

“Beware the Co-relation and Causality Delusions.”

Don’t be taken in by coincidences in the market.

Minor Axiom VIII:

“Beware the Gambler’s Fallacy.”

There is a gambling theory which suggests that one should put small stakes initially and test their luck, and if these turn out well one should go for big stakes on the dice table. But this is not correct. It only shows that winning streaks happen. But nothing is orderly about it. You can’t know how long it will last or when it will strike.

Sixth Major Axiom: On Mobility

“Stay away from putting down roots. They impede motion”.

You may feel socially comforting to have roots. But in financial life, roots can cost a lot of money. Have a flexible approach while investing. This axiom implies a state of mind.

Minor Axiom IX:

“Do not become trapped in a souring venture because of sentiments like loyalty and nostalgia.”

Do not develop emotional attachment to your investment. You should feel free to sell when desired.

Minor Axiom X:

“Never hesitate to abandon a venture if something more attractive comes into view.”

Never get attached to things, but only to people. Otherwise it hits your mobility. Never get rooted in an investment. You should remain footloose, ready to jump away from trouble or into a profitable opportunity as and when circumstances demand.

Seventh Major Axiom: On Intuition

‘A hunch can be trusted if it can be explained.’

A good hunch is something that you know but you don’t know how to recognise it. When a hunch hits you, try to locate some data in your mind for any familiarity. Then only should you act on it.

Minor Axiom XI:

‘Never confuse a hunch with a hope’.

Be highly sceptical. Examine every hunch with extra care.

Eight Major Axiom: On Religion and The Occult

‘It is unlikely that god’s plan for the universe includes making you rich’.

You can’t only pray that you should be made rich. You will have to work at becoming rich. Mere prayers will not suffice.

Minor Axiom XII:

‘If Astrology worked, all astrologers would be rich.’

This is self explanatory. Don’t trust predictions.

Minor Axiom XIII:

‘As superstition need not be exorcised, it can be enjoyed provided it is kept in its place.’

In your day-to-day financial matters, act rationally. But, when buying a lottery ticket, give it a full play to amuse yourself.

Ninth Major Axiom: On Optimism and Pessimism

‘Optimism means expecting the best, but confidence means knowing how you will handle the worst. Never make a move if you are merely optimistic.’

In poker and a lot of other speculative worlds, things are never as bad as they seem – most of the times they are WORSE.

Confidence comes not from expecting the best but from knowing how you will handle the worst. Optimism can be treacherous because it makes you feel good.

Tenth Major Axiom: On Consensus

‘Disregard the majority opinion. It is probably wrong’.

It is likely that the Truth has been found out by a few rather than by many.

Minor Axiom XIV:

‘Never follow speculative fads. Often, the best time to buy something is when nobody else wants it.’

This is the best way to get a good stock cheaply.

Eleventh Major Axiom: On Stubbornness

‘If it doesn’t pay off the first time, forget it’.

If at first you don’t succeed, try and try again and you will succeed in the end. This is good advice for spiders and kings but not for ordinary persons with regard to financial matters. Every trial is a costly error.

Minor Axiom XV:

‘Never try to save a bad investment by averaging down.’

If the price of the stock goes down after your purchase don’t buy more to bring down’ the average cost of your total holding. Investigate why the price went down rather than put good money in a bad bargain.

Twelfth Major Axiom: On Planning

‘Long-range plans engender the dangerous belief that the future is under control. It is important never to take your own long-range plans, or other people’s seriously.’

This is self explanatory and hence needs no comment.

Minor Axiom XVI:

‘Shun long-term investments.’

If possible try to stay away fro long-term investments. The author noticed that the Swiss group never took a long-term view of their stock purchases. They always sold out as soon as their targeted profit was achieved.

How to Stay Alert While Driving

How to Stay Alert While Driving

Driving drowsy is as dangerous as driving drunk. Numbers are hard to pin

down, but experts at the U.S. Department of Transportation put conservative

estimates at 40,000 injuries and 150 fatalities per year as a result of

drivers’ sleepiness.

Steps:

1. Get a good night’s sleep, and plan around your body clock so you drive

at the times of the day when you are most alert.

2. Take a 10- to 15-minute break to exercise, stretch or walk briskly

after every 2 hours you drive.

3. Let someone else do a share of the driving. Divide the driving into

blocks of no more than about 4 hours for each driver.

4. Eat regularly to keep blood-sugar levels even, but be mindful of what

you eat. A candy bar won’t help much once the initial sugar buzz wears off.

To stay alert, the body requires good nutrition.

5. Drink coffee or tea (or another form of caffeine) for a temporary fix.

Keep in mind that caffeine does not take the place of adequate sleep.

6. Don’t drink alcohol.

7. Avoid medicines that make you drowsy, including antihistamines, some

antidepressants, cold and cough medications, and some prescription

medicines. If the label warns, “Do not operate heavy machinery,” you are

being warned not to drive a car.

8. Learn to recognize drowsiness. Among the signs: You keep yawning, your

head nods, your mind wanders, you feel eyestrain, or your eyes want to

close or have trouble staying focused. It all means that you need a break

from driving.

9. Take a nap if you’re sleepy, even if you can’t get to a bed. You’ll

have to judge your surroundings, but you’re probably safer napping for a

half-hour in a locked car pulled over to the side of the road than you are

driving drowsy.

Tips:

Some drugs cause drowsiness for the first few days, so take extra care

when you start taking any new medicine.

Warnings:

If you ignore signs of drowsy driving, you not only put yourself at risk,

but also your passengers and everyone else on the road.

Watch for signs of a sleep disorder: falling asleep at inappropriate times

(such as at a movie theater), snoring loudly, feeling tired when you wake

up, or disrupting sleep because of breathing problems (a condition called

obstructive sleep apnea).

Careless driving cited for rise in fiery crashes

Careless driving cited for rise in fiery crashes

By Bassam Za’za’ and Alia Al Theeb, Staff Reporters GULF NEWS Published: October 07, 2007, 23:06

Dubai: Five people have been killed in separate traffic incidents in 24 hours, with three burning to death in a horrific crash yesterday.

Three people, believed to be two Colombians and an Omani, burnt to death in a collision on the Dubai-Al Ain road. A driver, believed to be Omani, was speeding in his four-wheel drive when he lost control and rammed into a car (carrying the other victims) which was parked on the shoulder ahead of the sixth interchange on the Dubai-Al Ain road. The accident took place at about 11am.

“The strong impact tossed the vehicles 98.1 metres before the three victims were burnt completely. The suspected Omani driver seems to have been fatigued, sleepy or was busy with something inside his vehicle when he lost control and rammed the other car. Investigations are ongoing to identify the victims and the causes,” Salah Bu Farousha, Head of the Traffic Public Prosecution, told Gulf News two hours after the accident.

No braking signs

The impact pushed the vehicles from the right-hand lane into the hard shoulder of the road before they were burnt completely, he explained.

Preliminary investigations showed that the driver of the four-wheel drive wasn’t paying attention as he did not try to brake but rammed into the other vehicle, Bu Farousha revealed to Gulf News. The Head of Traffic Public Prosecution called on motorists to refrain from parking their cars in a dangerous manner on shoulders of roads, especially on highways, without using warning lights.

In an accident on Saturday, a Russian woman driver ran over a man who was trying to cross Emirates Road. In a separate accident on Saturday, a motorcyclist was killed as he was speeding and riding his motorbike recklessly. As a result, he lost control and his motorbike skidded near Al Khawaneej Roundabout on the road toward Sharjah.

Dubai: Third fatal accident in about 10 days

This is the third major accident involving more than three casualties in about 10 days on Dubai roads. In the first accident, a minibus swerved on Emirates Road and seven workers from Thailand who had just arrived were killed on the spot.

The second accident happened in a Karama tunnel when a speeding car hit the kerb and overturned.

The car exploded in flames and burnt within 90 seconds, killing five men in it.

Webometrics Ranking of World Universities

Webometrics Ranking of World Universities

Indira Gandhi National Open University (IGNOU) has been ranked 17 out of top 100 in the Indian Subcontinent Region in “Webometrics Ranking of World Universities”, a leading international website http://www.webometrics.info.

IGNOU, a distance educational institution has competed with conventional institutions like IIMs, IITs, Anna University, University of Pune, University of Delhi, AIIMS, B.H.U. and Open University of Sri Lanka, Virtual University of Pakistan, North South University, Bangladesh, University of Dhaka etc.

The Universities are classified by a mathematical combination of the rankings according to their websize, number of rich files, number of papers published in the last years and records in the Google Scholar. The criteria combined include link visibility, number of citations to papers in the IST database and number of visits (popularity) to the web domains.

The methodological section adheres the Berlin Principles on Ranking of Higher Education Institutions.

Although the main primary of the Webometrics Ranking is to promote the publication in the web by Universities and other research related institutions, the web indicators produced allow a comparative analysis with other scientometric or bibliometric indicators. The data shows both a global good agreement among rankings and several striking measurements corresponding to a well defined group of countries.

The aim is to show the commitment of these organizations to the electronic publications. The purpose is to offer an extended coverage including information about countries institutions.

This Ranking is being published since 2004 on a regular basis using the web data as indicator of the visibility and impact of the activities of the universities, colleges and research institutions worldwide.

Awareness-cum-Training Packages in Disabilities

Awareness-cum-Training Packages in Disabilities

Indira Gandhi National Open University (IGNOU) has signed an MoU with Rehabilitation Council of India (RCI) to make joint efforts in promoting and implementing extension training and education programmes for the empowerment of the special target groups of people with disabilities.

The agreement was signed by Mr. K Laxman, Registrar, IGNOU and Dr. J. P. Singh, Member Secretary, RCI in the presence of Prof. V.N. Rajasekharan Pillai, VC IGNOU and RCI, Chairman Maj. Gen (Retd) lan Cardozo.

IGNOU will collaborate with RCI in programme design and development of special education and rehabilitation programmes through multimedia distance mode and will also facilitate delivery and certificate of such programmes.

This Awareness cum Training programme of 3 months for parents will be upgraded to a Certificate/ Diploma level programmes for the parent’s willing to upgrade their knowledge and having a minimum qualification as decided by experts. This will be a self-viable programme.

It will ensue the translation of the study material for the programme in 8 languages namely Gujrati, Marathi, Malayalam, kannada, Oriya, Bengali, Tamil & Telugu and launch in all the 8 languages within 6 months.

IGNOU & RCI will launch/implement B.Ed/ M.Ed. (Special Education) & PGPD (Special Education) at the places where the State Open Universities are not functioning.

An audio-visual based motivational extension programme with the objective of apprising the parents of the potential of children with special needs and advising them on possible sources of useful information on the education and rehabilitation of children with disabilities will be developed.

A Brief about IGNOU-RCI MoU

An MoU was signed between Indira Gandhi National open University and Rehabilitation Council of India on 18th September, 2007 which would be valid for a period of five years. Under the MoU, IGNOU & RCI will collaborate in programme design and development of special education and rehabilitation programmes through multimedia distance mode and will also facilitate delivery and certification of such programmes. The Degrees/Diplomas/Certificates under this MoU shll be awarded jointly. RCI recognizes IGNOU as the Apex National Resources Centre for Special Education and Rehabilitation Programmes through Distance Mode. RCI will also extend technical expertise to the IGNOU and its study centres. The study centres of IGNOU and training centres of RCI all over the country will provide academic help through tutorials and counseling, through books and other audio visual material specially prepared by the IGNOU in collaboration with RCI

Great investing tips from Rakesh Jhunjhunwala

Great investing tips from Rakesh Jhunjhunwala

Great investing tips from Rakesh Jhunjhunwala

“Markets are like women — always commanding, mysterious, unpredictable and volatile,” quipped ‘Big Bull’ Rakesh Jhunjhunwala (inset) while addressing a meet organised by Shailesh J Mehta School of Management, IIT, Bombay on August 10.

A champion broker, often termed as Warren Buffett of the Indian stock market, Jhunjhunwala had a full-to-the-brim auditorium spellbound as he traced how he made his fortune from a starting capital of Rs 5,000. His career path is stuff dreams are made of.

What earned him fame is his skill to pick under-valued stocks. Some of his renowned calls are Karur Vysya Bank, CRISIL and Bharat Electronics. There are, however, quite a few more. Talking about his company RARE (derived from the first two letters of his name and that of his wife Rekha) Enterprises, Jhunjhunwala says, “My company has only one client — my wife — so that I don’t need to handle others’ money.”

One of the biggest bulls of the Indian market, Jhunjhunwala believes in trading by the hunches. “If in doubt, listen to your heart,” is what he tells young investors. Extremely optimistic about India’s growth story, Jhunjhunwala shared with his audience some valuable insights about the Indian economy, future of Sensex. Read on.

Rakesh Jhunjhunwala’s secret to success

What paved the way to Jhunjhunwala’s success?

A democratic growth process rather than an imposed one and a biological evolution, pat comes the reply.

He owes a lot to resurrection of a dormant and vigorous entrepreneurial gene of India. “The country has rediscovered its confidence.”

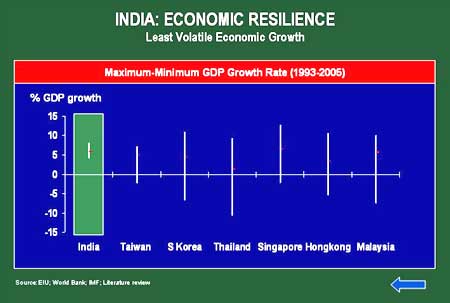

There has been a strong improvement in India’s macroeconomic indicators, combined with a robust banking system.

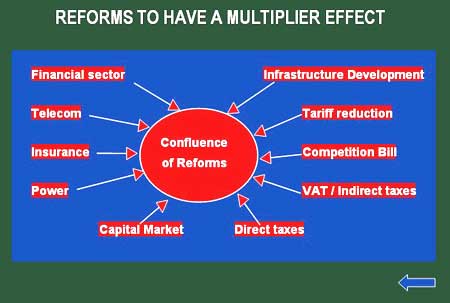

Improvement has also been observed in India’s corporate performance, powered through productivity gains. Jhunjhunwala is convinced that on-going reforms would have a multiplier effect on India’s economy.

Jhunjhunwala’s investment strategies

Jhunjhunwala learnt investment strategies the hard way. And he was more than willing to share it with his audience. Here are a few gems from his book of learning

* Necessary for any investor is optimism.

* Be opportunistic but wait for the right moment

* Study the market thoroughly. Refer to history

* Maximise profits and minimise losses

* Invest in a business not a company

* Always have an independent opinion. Observe and read relevant information with an open mind

* Be happy with your gains but learn to accept losses with a smile

* Be prepared for challenges and risks

Predicting a brighter and better future for the Indian markets, Jhunjhunwala signed of by saying that the Indian markets will reach the peak by 2010.

Gems from Jhunjhunwala

For beginners in the market, here are a few invaluable gems from Jhunjhunwala’s book:

* Whatever you can do or dream you can, begin it. Boldness has genius, power and magic in it.

* Do something you love

* The means are as important as the end

* Aspire, but never envy

* Be paranoid of success — never take it for granted. Realise success can be temporary and transient

* Build a fighting spirit — take the bad with the good

* When you see a horizon, it seems so distant. When you reach that horizon, you will realize how many more horizons are within reach

5 things you need to be successful

Asked how much patience should an investor have, Jhunjhunwala said, “Get married and you will understand how patient you need to be.”

“Patience may be tested, but conviction will be rewarded,” he asserted. He appealed to the budding investors to go by what George Soros said: ‘It’s not important whether you are right or wrong, it more important how much you lose when you are wrong and how much money you make when you are right.’

To be successful in investing, five things are critical. There has to be:

* an attractive, addressable, external opportunity;

* a sustainable competitive advantage;

* scalability and operating leverage; and

* a qualified and integral management

* Last but not least, it is of vital importance what one buys and at what price.

‘India has everything’

Rakesh Jhunjhunwala believes that India has all ingredients that the stock markets value and hold in high regard. Some of them are:

* Efficient capital allocation

* Sustained earnings expansion driven by growth and productivity

* 8 per cent+ real GDP growth + 4%+ Inflation = 12%+ Nominal GDP growth

* Corporates to grow faster than unorganised sector

* Operating and financial Leverage to kick-in

* Corporate earnings to grow at 18%+

* Favourable framework for equity investing

* Rising savings, yet low equity ownership — significant potential

* Corporate governance

* Transparency

* Effective regulation

* Electronic trading

* Dematerialisation

* Tax paradise for equity investing under the STT regime

‘Be realistic’

Jhunjhunwala also spoke about his beliefs that made a case for sustaining the India growth story.

He said enormous wealth was created over the last five years because opportunities in India have grown manifold.

Admitting that gains were going to be moderate in future unlike the manifold rise over the last few years, he advised investors to be realistic in their expectations.

‘The market is always right’

Jhunjhunwala takes the cue from Warren Buffett’s words: “Most people get interested in stocks when everyone else is. The time to get interested is when no one else is. You can’t buy what is popular and do well.”

“Blindly following stock picks by big investors is not a wise thing to do,” he warns investors. “I don’t think the government is necessarily interested in hurting growth. The government is interested in growth with controlled inflation.”

“The market,” he says, “is always right. Markets cannot be taught, they have to be learnt.”

“We must have an attitude where we must balance fear and greed,” was the hot tip by one of India’s most high-profile investor.

Why growth will continue

Speaking on the strength in India’s fundamentals, Jhunjhunwala elaborated on forces that would sustain the growth momentum.

According to him, growth enablers (such as favourable demographics, higher base of skilled people and education base), liberalisation catalysts (such as competition), fall in interest rates, multiplier effect (on account of reforms), structural changes in quality of corporate earnings and micro trends (such as change in mindset of companies who are aspiring to become global) are likely to drive India’s growth story to a higher level.

Text, courtesy: RARE Enterprises and Shailesh J Mehta School of Management, IIT, Bombay

Want to succeed? Avoid these 9 traps

Want to succeed? Avoid these 9 traps

Robert J Herbold

Success leads to the damaging behaviors of a lack of urgency, a proud and protective attitude, and entitlement thinking. This leads to the tendency to institutionalize legacy thinking and practices. Essentially, you believe that what enabled you to become successful will enable you to be successful forever.

After reviewing this problem in many companies, I believe there are nine dangerous traps into which successful people and organizations often stumble.

Trap 1: NEGLECT

Sticking with Yesterday’s Business Model

By business model, I mean what you do and how you do it. It includes such issues as deciding what industry you will be competing in and what approaches you will use in carrying out all the processes necessary to compete in that industry. Will we manufacture something or contract it out? How will we sell our products or services?

Do we go through retail channels? How should we organize our sales force? Which segments of the industry do we want to ignore, and which do we want to compete in? What is the structure of our support staff? Which parts of the organization do we out source? What are our approaches to distribution and inventory management? What are the cost targets of the various components of the organization, like information technology costs and human resources costs? Does our model leave us satisfied with our gross margins, profit margins, and other such figures?

Organizations should be consistently reviewing all aspects of their business model, looking for areas that are weak and need to be overhauled. By weak, we mean out of date, too costly, too slow, or not flexible. In which areas of the business model are you at parity? In those areas, are there any bright ideas on how to achieve a competitive advantage?

TRAP 2: PRIDE

Allowing Your Products to Become Outdated

You may be super proud of your product or service today, but you have to assume that it is going to become inferior to the competition very soon. You need to hustle ad beat your competition to that better mousetrap, and you need to do it over and over.

The amazing thing about success is that it leads to a subconscious entitlement mentality that cause you to believe that you no longer need to do all the dirty work of getting out and studying consumer behavior in details, analyzing different sales approaches, jumping on the latest technology to generate improved products, and everything else that is required to stay ahead. The attitude is often one of believing that you have done all of that and have figured it out, and now things are going to be fine.

Until the early 1970s, typewriters were used to prepare documents. The IBM Selectric model was the standard. Then along came Wang Laboratories’ word processor in 1976, providing a completely new approach. It displayed text on a cathode ray tube (CRT) screen that was connected to a central processing unit (CPU). In fact, you could connect many such screens to that CPU in order to handle many different users. Wang’s device incorporated virtually every fundamental characteristic of word processors as we know them today, and the phrase word processor rapidly came to refer to CRT-based Wang machines. Then, in the early to mid-1980s, the personal computer emerged. Wang saw it coming but made no attempt to modify its software for a personal computer. PC-based word processors like WordPerfect and Microsoft Word became the rage, and Wang died. Wang fell into the trap of not updating its products, even though it basically invented the word processor industry.

We saw this behavior very clearly with the General Motors example. Its cars, while highly distinctive back in the 1970s, were allowed over time to look more and more alike, and the excitement factor for the customer disappeared.

TRAP 3: BOREDOM

Clinging to Your Once-Successful Branding after It Becomes Stale and Dull

Constantly achieving uniquencss and distinctiveness for a brand and also keeping it fresh and contemporary is hard work. Once a brand achieves some success, the tendency is to sit back and pat yourself on the back, allowing your brand to become dull and ordinary.

The Plymouth automobile was introduced by Chrysler for the 1928 model year as a direct competitor to Ford and Chevrolet. It was a sturdy and durable car that attracted a legion of loyal owners. Plymouth became one of the low-priced three from Detroit and was usually number three in sales, just behind Ford and Chevrolet. For almost two decades, Plymouth sold almost 750,000 cars per year and had a solid brand reputation in the low price range of being reliable but having a bit more flair than Chevrolet or Ford. Older readers may remember the 1957 Plymouth with the huge fins, as well as its Road Runner (beep beep!) model. Plymouth had a very clear brand positioning.

In the 1960s, the Plymouth brand began to lose its uniqueness. Chrysler decided to reposition the Dodge, reducing its price so that it was quite close to Plymouth’s. Chrysler came out with low-priced compact and intermediate-size models under both the Plymouth trademark and the Dodge trademark. By 1982, Dodge, was outselling Plymouth. Throughout the late 1980s and the 1990s, Plymouth offered nothing unique. Sales continued to decline, while Dodge was quite healthy. In 1999 Chrysler announced that the Plymouth brand would be discontinued. The lesson is simple: when you allow brands to get stale, they die.

TRAP 4: COMPLEXITY

Ignoring Your Business Processes as They Become Cumbersome and Complicated

Successful organizations often reward themselves by adding more and more people and allowing processes to become fragmented and nonstandardized. This is often done under banner of refining the management of the business. It is also caused by business units and subsidiaries seeking more autonomy, which leads them to develop their own processes and staff resources. Before you know it, getting any kind of change made is very complicated.

Over and over again you read stories about organizations experiencing weak financial results, then finally coming to grips with the problem, laying off thousands of people and simplifying the organization.

We saw in our Toyota case study how aggressive that company is at constantly improving each and every process. Keeping that mindset of constant improvement is very difficult. Success usually leads to a decrease in the intensity with which you tackle such challenges. Also, success leads to a belief that since we are doing so well, we probably need to reward the people in the organization who are asking for their own building and lots of extra people to get them to the next level. Importunely, all those extra costs often lead to bloated processes and further fragmentation of how work gets done.

TRAP 5: BLOAT

Rationalizing Your Loss of Speed and Agility

Successful organisations and individuals tend to crate complexity. They hire a lot of extra people, since clearly things are going well, and those people find things to do, often creating layers of bureaucracy, duplicating capabilities that already exist in the organization, and making it very hard to react quickly to change.

Getting an organization to constantly think about retaining simplicity and flexibility is not easy. The account given in the previous chapter of Toyota’s Global Body Line is a good example of doing it right. Toyota thought about agility ahead of time, and when it came time to build a brand-new car, such as the Prius, it didn’t have to build a new plant or a new line. This enabled Toyota to get to market fast and save tens of millions of dollars compared with traditional approaches.

TRAP 6: MEDIOCRITY

Condoning Poor Performance and Letting Your Star Employees Languish

When organizations are successful, they have a tendency to stop doing the hard things, and dealing with poor performance is a really hard thing. It also becomes hard to move new people into existing jobs, because there is the burden of getting the new person up to speed and the perception that you are losing valuable expertise. Also, the really strong performers and to get ignored. Consequently, what happens in many successful organizations is that people are left in their jobs too long and poor performance is not dealt with as crisply as it should be. Unfortunately, this also leads to strong players not being constantly challenged.

Successful organizations are especially vulnerable to this trap, since companies that achieve success often have high morale and pride. And who wants to spoil the fun by dealing with the tough personnel issues, which is an onerous task for most managers? Any excuse to put it aside will be embraced.

TRAP 7: LETHARGY

Getting Lulled into a Culture of Comfort, Casualness, and Confidence

Success, and the resulting tendency to become complacent, often leads organizations and individuals to believe that they are very talented, have figured things out, have the answers to all the questions, and no longer need to get their hands dirty in the trenches. They lose their sense of urgency � the feeling that trouble might be just around the corner.

Considering our case studies on GM and Toyota, the contrast between their cultures is really striking. GM seems to exude pride and an attitude of “we are the real pro in the industry,” while Toyota has a more humble personality that is all about constant improvement.

The leader of a group really sets the tone on this cultural complacency issue. The tendency is to become very proud of your success and protective of the approaches that got you there. It is those very tendencies that lead to an insular, confidence culture that makes people believe that they are on the wining team, while in reality, the world is probably passing them by.

TRAP 8: TIMIDITY

Not Confronting Turf Wars, Infighting, and Obstructionists

Success often leads to the hiring of too many people and the fragmentation of the organization. Business units and subsidiaries work hard to be as independent as possible, often creating groups that duplicate central resources. Staff groups fragment as similar groups emerge in the different business units. Before long, turf wars and infighting emerge, as who is responsible for what becomes vague.

Even worse, the culture gets very insular, with an excessive focus on things like who got promoted, why am I not getting rewarded properly, and a ton of other petty issues that sap the energy of the organization.

Another source of turf wars and infighting is lack of a clear direction for the organization and slow decision making on critical issues. When these kinds of management deficiencies occur, people are left to drift and end up pulling in different directions. That often leads to tremendous amounts of wasted time as groups argue to have it their way.

TRAP 9: CONFUSION

Unwittingly Providing Schizopherenic Communications

When an organization is success or stable, its managers often fall into the trap of not making it clear where the organization is going from there. Sometimes this is because they don’t know, but they don’t admit that, and they don’t try to get the company’s direction resolved. They do everything they can to keep all option open, with no clear effort to get decisions made and a plan developed. Such behaviors lead to speculation by the troops, based on comments that they pick up over time. Often those comments are offhand remarks that the leaders have not thought through. Or the troops hear conflicting statements coming form a variety of folks in leadership positions in the organization.

When employees receive confusing and conflicting messages and don’t have a clear picture of where the organization is gong or whether progress is being made, they feel vulnerable and get very protective of their current activities. In late 1991, IBM’s CEO,John Akes, announced that in the future, IBM would look more like a holding company and that “clearly it’s not to IBM’s advantage to be 100 per cent owners of each of IBM’s product lines.”

During the next 12 months, everybody was trying to figure out what he meant. And IBM made no attempt to start publishing separate financial information by product line in preparation for possible spin-offs. IBM also ignored Wall Street’s suggestion that it create separate financial entries, with their own stock exchange symbols, for the products that were to be spun off. Employees and investors were confused. The IBM board of directors finally ended the drama in early 1993, announcing that Akers was leaving and a new CEO would be hired quickly. From 1987 to 1993, IBM shareholders lost $77 billion of market value.

Communications from the head of the organization, be it a small group or an IBM, are critical. People want to know where they are headed and how things are going. When the words and actions don’t match, confusion reigns.

In the remaining parts of this book, I will discuss these traps in detail. In each part, I will give detailed examples of companies and individuals that in some cases have been hurt and in other cases have avoided these problems. My objective in each part is to provide specific actions that people can take to avoid the particular trap, or to rid themselves of the problem.

Excerpted from:

Seduced by Success by Robert J Herbold.

Copyright 2007 by Robert Herbold. Price: Rs 495. Reprinted by permission of Tata McGraw Hill Publishing Company Limited. All rights reserved.

Robert J Herbold was hired by Bill Gates to be chief operating officer of Microsoft Corporation. During his seven years as COO of 1994 to 2001, Microsoft experienced a four-fold increase in revenue and a seven-fold increase in profits.

Gulf funds drift away from dollar

Gulf funds drift away from dollar

By Babu Das Augustine, Banking Editor GULF NEWS Published: October 07, 2007, 00:04

Dubai: Asset diversification by the Gulf sovereign wealth funds and the possibility that the Organisation of Petroleum Exporting Countries (Opec) will change the pricing of oil from the dollar to another currency could mean more trouble for the dollar.

The dollar has been losing its charm as a reserve currency due to its persistent weakness against a host of other international currencies.

The September non-farm payrolls report on Friday showed 110,000 jobs were created in the US last month. Although the dollar reacted positively to the news and gained initially, the rally quickly fizzled.

Amid the dollar’s free fall following the half per cent interest rate cut in September, Qatar last week said its $50 billion sovereign wealth fund has cut its exposure to the dollar by more than half to about 40 per cent of its portfolio.

“While the opportunities are growing, the risk levels of Asian assets have come down substantially in recent years,” Ronnie Chan, chairman of Hang-Lung Properties Hong Kong, told Gulf News recently.

Analysts see the admission by Qatar as a signal that regional state-owned funds are moving away from the dollar.

Oil pricing

“Qatar has admitted that its investment fund has been diversifying their portfolios to compensate for the decline of the dollar. It would be naive to think that other Gulf funds are loyal to the dollar at the cost of heavy portfolio losses,” said a Dubai-based investment banker.

During the past 12 months, companies, mainly state-owned investment arms and private equity firms from the GCC, have quietly acquired more than $50 billion in assets worldwide with Asia’s and Europe’s shares together accounting for more than 55 per cent.

The state-owned Kuwait Investment Authority, with assets of more than $150 billion, last year increased the Asian share of its portfolio to 20 per cent from 10 per cent.

Although gulf central banks have been discussing asset diversification in the past two years, there hasn’t been any evidence of a major shift. The size of assets held by Gulf central banks are relatively small compared to the funds managed by the state-owned investment funds.

According to IMF estimates, global investment funds managed by governments control an estimated $2.5 trillion, outstripping hedge funds. Morgan Stanley estimates these assets could rise to $12 trillion by 2015, roughly the size of the US economy. Gulf countries account for a major share of these funds.

Currency market analysts believe that the gulf sovereign funds’ gradual move away from the dollar is a precursor to Opec opting for a different currency in which to price oil.

“If the dollar were to lose its lustre as a reserve currency this could prove disruptive to the global financial system,” Merrill Lynch said in a research note.

“Pricing oil in dollars might have made sense when there was a paucity of other relatively stable currencies and when the Middle East imported more from the US – but not any-more,” said an analyst.

You must be logged in to post a comment.