Information – Money Market

News Update: Coronavirus: Abu Dhabi suspends rental evictions, freezing bank accounts

The move is in line with UAE’s keenness to support members of society and reduce their burdens during the current situation.

His Highness Sheikh Mohamed bin Zayed Al Nahyan, Crown Prince of Abu Dhabi and Deputy Supreme Commander of the UAE Armed Forces, on Monday directed the Abu Dhabi Judicial Department to halt all rental property eviction cases currently underway, along with executive procedures like imprisonment, blocking of bank accounts, seizure of vehicles, stocks and assets for a period of two months.

The decision exempts cases related to alimony and labour disputes.

The move is in line with the UAE government’s keenness to support members of society and reduce their burdens during the current situation.

Source: Khaleej Times

A recent discussion on recession and it’s affects

A recent discussion I came across on recession. Thought of sharing it with you.

*******

A reply to it:

Thank you for the mail on actionable insights to prepare for the

recession. I wish to differ on certain points mentioned by the

“financial consultant”

First of all, Recession means different things to each person as a

Businessman, Investor or employee

To the Investors, it is the best time to buy (or invest). During

recession precious land becomes affordable, cost of construction

becomes less. So if you, as an investor is planning to invest in a new

project that involves construction works, this is the best time. This

is becuase, a typical construction of mall, factory or a resort takes

about 1.5 to 2 years in India. The recession will be over in say 1-2

years. So your new business will be opening up at a time when the

economy is recovering. And if you are planning to invest in already

established businesses (instead of new ventures), this is still a good

time. This is because, in good times the promoters of this business

will ask you for a heavy goodwill amount. In recession, even the best

companies may have cash flow problems and may be willing to bring in

equity at investors terms. And once the recession is over, these

companies will get back to form. (Recession has happened many times,

infact it is a cycle, so dont think of recession as a Tsunami that

wipes out everything).

To the businessmen, recession can be a bad time or a good time, based

on what thier position is. To begin with there are some industries

that do good when others do badly. You just have to search out for

those sectors. Recession can be bad to a business that has heavy

overheads and its business is dependant on other businesses which

might get a bad kick from recession. Businesses with good cash

reserves should hold on to thier cash, as they can expect red figures

in the profit loss account for few months to come. It is a good time,

for them to eliminate fat (both in terms of bad staff and unproductive

assets). When the times are good, businesses seldom care about best

practices and efficiency. I was involved with a factory during a

downturn period, and in order to survive, we had to take extreme

measures with regards staff management, implementation of new

machineries and all kind of best practices (much aganist our will) to

survive. To finance these we had to merge with a competitor as well.

Bad times made that business so strong, that in 2008 (when the global

economy calls it a bad year), they made a record profit and became

market leader in thier sector. So if we take the recession properly,

it is a good time, to make a business strong.

To the Employees, recession can be good and bad, again. Lazy and

unproductive employees will have a hard time holding on to thier jobs

and in case they lose thier jobs, it will be difficult to get a new

one. One good thing about employment market during recession,

especially in India, is that I am hoping to see “job hopping” slow

down. But recession is a good time, for loyal, hardworking staff to

show thier worth to the company. By working more than others, by

accepting mangement decisions, by perhaps sacrificing bit of thier

salaries, these employees can show to management, they are soldiers

they can count on. And they will be most visible. These employees,

have a better chance to get promotions and upgradation in salaries

during the good times.

My comments where I disagree to the previous mail, are ;

1. Dont sell your stocks, if you can afford to keep them for 1- 2

years. Most of the stocks are now trading below thier intrinsic value.

By selling them at loss now, you will buy them at even higher cost

later on. So hold on to them. Put your shares in locker and go to

sleep. Wake up after 2 years, to see its price. On a different note, I

dont recommend day trading to anyone, its almost like gambling. With

stocks you should buy and sell, with long term view.

2. I dont agree to not investing, for reasons I have mentioned above.

3. Dont sell your assets now, the price is Below its real value. Wait

for 2 years for boom to start again.

This are my views. About me, I am the CEO of a Venture Consulting firm

based in Calicut (Kerala). I did my masters in Finance and Investment

from Exeter University, UK. I have been in Gulf for many years. I had

worked at german strategy advisory firm (Dubai), as consultant.

At Capella, we advice investors on investing in various of projects,

by conducting business research, preparing project reports, business

plans, business counselling and venture project management.

Forwarded e-mail

As forwarded by a financial consultant, in Dubai.

>> *Recession is coming… make your own judgment, don’t panic! Do

what is wise.

The recession looks very eminent. It is really time to take pro active

steps to avoid a painful time in the next two years which is how long the

recession is expected to last.

> Suggestions:

> 1. Don’t take any loans; buy homes, properties with loans, or even cash. Keep as much cash as possible.

> 2. Pay off as much of personal loans, private loans, as debt collection

will be hastened.

> 3. Sell any stocks you can even at lower prices.

> 4. Take money off from Trust Funds.

> 5. Don’t believe in huge sales forecast from customers, be extremely

prudent, lowest inventories, reduce liabilities.

> 6. Don’t invest in new capital.

> 7. If you are selling homes/ properties/ cars, do it now, when you can get good prices, they are going to fall.

> 8. Don’t invest in new business proposals.

> 9. Cancel holiday plans using credit cards.

> 10. Don’t change jobs, as companies will retrench based on ‘last in first

out’.

Stay cool, wait, and if you took all of the above actions and more, you

probably will be better off then many. This is not a rumor.

Bear Stearns is the first of many banking and financial institutions that

will start falling in the not too future. If Bear Stearns can fall, so can

JP Morgan, Citibank, HSBC, and the whole world. US economy falls, the rest will crumble.

India and all those self economies will be the most protected, but not

gullible.

Europe may be a little stronger, but not China, another giant place!

Malaysia will see significant impact.

> Be alert and pass this to your friends!!!*

Price to book value numbers could help you in crisis

Price to book value numbers could help you in crisis

28 Oct, 2008,Amriteshwar Mathur, ET Bureau

MUMBAI: What is a good yardstick for an undervalued stocks in times of crisis such as the current one? The answer to that, many market watchers say, is price to book value(P/BV). Book value is the measure that each shareholder stands to get, were the company to be liquidated.

Conventional wisdom suggests that there is very little chance of going wrong if an investor were to put his money in a stock with a P/BV of less than one. Already 21 stocks in the BSE-100 index have seen their price to book value fall below one, as a result of the unprecedented erosion in their stock prices.

Stocks that fall into this category include PSU oil marketing companies like HPCL and IOC, and metal stocks like Tata Steel, Hindalco and JSW Steel.

In the case of oil marketing companies, the recent softening of crude oil prices has not helped much. For one, they are still holding inventory purchased at very high prices. Also, these companies also have refining divisions, which are the major contributors to their profitability. Gross refining margins have fallen sharply in line with the slide in regional refining margins, and is likely to weigh on earnings.

In the case of metal stocks, investors are concerned that a global economic slowdown over the next few quarters could adversely hit demand for commodities in general.

Similarly, investor concerns for the growth prospects of the real estate, cement and construction sector over the medium term has resulted in scrips like Grasim Industries and IVRCL Infrastructure & Projects quoting at a price to book value of less than one. At Monday’s close of 4343.2, the broader BSE-100 index trades at a P/BV of 2.06 times.

Says Ramdeo Aggrawal, managing director, Motilal Oswal Financial Services, “Investors would need to look at the fundamentals of each sector over the medium term where stocks are trading at a price to book value of less than one, and decide if there are growth possibilities at the current stock prices.”

Adds Anuj Choksey, co-head, institutional equities, KR Choksey Shares and Securities, “Valuations of metals shares and those connected to the construction sector are trading at ridiculously low levels as investors are assigning pessimistic valuations at the first signs of a slowdown.”

Meanwhile, the Sensex went below 8,000 intra-day on Monday, as there was no let-up in the selling fury that has gripped Dalal Street over the last couple of weeks. This has been a hallmark of emerging markets in general. So how does India compare with them? At Monday’s close, the Sensex is trading about 9.5 times trailing 12-month earnings.

In contrast, other indices like the Shanghai Composite Index ended at 1,723 on Monday trade at a P/E of 13.35 times, while the Brazilian Bovespa at Friday’s close of 31,481 is trading about 7.5 times. Of course, the Russian stock market index, the Russian RTS Index which has lost nearly 70% since its peak over the last few weeks, trades at an abysmal P/E of 3 times.

20-25% chances of Sensex stooping to 11K

20-25% chances of Sensex stooping to 11K

Ridham Desai for Money Control.com

Ridham Desai, MD and Co-Head-Equity, Morgan Stanley feels that one is likely to see more downside before market bottoms out and there’s 20-25% probability of the Sensex going down to 11,000. The market may take some more time to form a bottom, Desai said. He alsosaid that, the price correction shows that India may be in a bear market. Desai said that, most indicators show that the market is in a ‘fear zone’. On a more positive note, he affirms that the market may see an end to the pain by the third quarter of this year

Desai is skeptical about whether companies will disclose their losses this quarter. He feels that the valuation gap between sectors needs to narrow down. He further added that if India falls another 10-15% as against other emerging markets, it will create a buying opportunity.

“It has not satisfied the time requirement because bear markets usually are longer. It has definitely satisfied the price correction requirement. We have been through a couple such corrections in this bull market. If this is not a bear market then it could turnout to be like May 2004 or 2006 when we went through a similar type of price corrections. This time around, the fundamentals are under the scanner and that’s what makes me feel that this is a bear market. We may have a little bit more time to go before we get to that so-called bottom,” he added.

Excerpts from CNBC-TV18’s exclusive interview with Ridham Desai:

Q: Are we in a bear market?

A: It looks like one. It has not satisfied the time requirement because bear markets usually are longer. It has definitely satisfied the price correction requirement. We have been through a couple such corrections in this bull market. If this is not a bear market then it could turnout to be like May 2004 or 2006 when we went through a similar type of price corrections.

This looks more like a bear market because the fundamentals in 2004 and 2006 were different. In May 2004 and 2006, the macro was pretty much intact and we got some global surprise which has caused markets to correct in terms of valuations. We found a bottom very quickly and the markets rallied all over again. This time around, the fundamentals are under the scanner and that’s what makes me feel that this is a bear market. We may have a little bit more time to go before we get to that so-called bottom.

Q: What’s your definition of a bear market? There are many definitions, some say a 20% fall is enough for a bear market, but obviously you define it differently?

A: 20% is one criteria, another criteria would be the 200-DMA. From 2003 till now, we have had only one penetration of the 200-DMA and that too for a very brief time in 2004.

Q: This time we are consistently below it.

A: Yes, we are consistently below it. One should look at is falling intermediate tops and bottoms. That’s another thing that was not met in the previous two corrections of 2004 and 2006. In that there were one or two falls and then the market actually did not establish lower bottoms. This time we are getting consistently lower bottoms and tops. So, that feels like a bear market if you look at the long-term trend lines.

I am not a big believer in trend lines because you can draw many lines through two points and justify a lot of things on trend lines. But these are the three things that I look at. The percentage of fall, are successive tops and bottoms lower or higher, and how long we stay below that 200-DMA? The percentage of fall at 20-25% is a good number. We have at least three bottoms which have been lower than the 200-DMA and have been staying below that for a while.

Q: Is history a good guide to how long bear markets typically last or have things changed because one contention has been now-a- days that the bear markets are much shorter, so we don’t need to worry about 4-6 quarters it will all get over in two quarters?

A: There were three bear markets since the early 90’s. We had the Harshad Mehta scam-related bear market that lasted approximately 50-weeks and the fall was about 50%. Then, we had the mid-90’s emerging market sell-off, which produced 55% fall and lasted about 86-weeks. Last, we had the tech bubble where the price fall was approximately 50%, but it lasted longer. It took 110-weeks for the markets to bottom out.

This is what distinguishes this time from the previous and this is debated quite hotly because this is intuition rather than based on any facts or data. India has moved on structurally, we are not the same economy that we used to be in the 90’s. Therefore, to argue for a100-week prolonged bear market like we had gone into during the tech bubble days or in the mid-90’s will be a little bit too aggressive.

We will probably get a 50% fall if this turns out to be a bear market. In terms of depth, you will still get that 50% fall and several parts of the markets are already down 50%, so we are getting there. In terms of length, we will not get the type of the 90’s bear market that we got, so this will be shorter. May be it will last for another 15-weeks but it won’t establish the 70-80-90 week period that we have seen in the past.

Q: What would convince you that it is a bear market? You are saying it could be a bear market, which you think is likely. But it could also be a deep correction in a bull market. What would utterly convince you that this is a bear market that we have entered?

A: From a fundamental perspective, it is earnings because bear markets never come with earnings rising and that too at a base of 20-25%, which is what we have all got used to. Even in the early and late 90s, we got earning declines. So, maybe we don’t get earnings declines but get a slowdown in earnings. So, that is one thing we need to watch out for. When earnings start declining, we know that it is a bear market. So, that is fundamental.

Technically, I am kind of more or less convinced. There is not much room left because the market breadth has collapsed, midcap index has collapsed, several sectors with fluff have gone away, and the momentum stocks have gone away. We have discussed this 200-DMA, the tops and bottoms have fallen. So, I cannot imagine that there is much of a debate there.

The debate will be on the earnings and fundamentals. Have they peaked or is this just a mild correction and we are going to recover pretty quickly? So, if that is going to now fall then this is a bear market.

Q: The scary bit is the 50% number that you are working with. In past bear markets, we have fallen 50% from the top.

A: Yes, we have fallen 50% or slightly more.

Q: Is it likely then that we will go back from that 21,000 peak to something like 10,500-11,000?

A: We need two conditions to get there. First, we need some extensive turmoil in global financial markets beyond what we have already had. We need some more things to happen, maybe Europe will get into trouble, or may be non-financials in America will get into trouble. We need that because without that I do think India on its own is going to slip into a 50% correction. Second, we need a policy mistake at home.

It is a challenging time right now. Growth is slowing down, inflation is rising, and it is an election year. These conditions are similar to 1996 when growth had peaked out, inflation was rising, and we were in election year. If there is a rate hike, or there is a response from the policy side which accentuates the growth slowdown, then we could argue for a 50% correction. Otherwise, we may miss that precise 50% point and may bottom out before that.

Q: What kind of a probability would you attach to it happening?

A: A 20-25% probability of the Sensex going to 11,000. We will probably bottom out before that.

Global financial market conditions may not worsen dramatically from here. It may spread a bit in the US. In the US, the pain in the financial sector is probably behind us. We may get some pain in non-financials, industrials, and materials notably. In Europe, we may see a bit more pain because they have not really seen that pain. But it may not be a catastrophe. It may not be like what we saw in the US, it may not be like a Bear Stearns effect. We have seen some pain come out in the last one week and the markets have responded well to that. So, we may get a bit more pain, but nothing of the nature that we need to take the markets down another 20-30%.

At home we look okay. We are getting some response from the government, which is the right response in the circumstances. So, we don’t want the central bank to come around and say okay, inflation is high so let me hike rates because our own view is that rates are already prohibitively high. They are already in restrictive zone, and they need to be lower. If you hike them further, then growth will probably fall even harder and that will create a problem for the markets here. It will be hard to recover from those lower levels later on. So far, as we don’t do that, I feel confident that we may not do that. I think we should be okay.

So, we may not get to 11,000, but it is still a one in a four chance. We may bottom out before that.

Q: It is a general feeling in many quarters that we may have in some sense established a near-term bottom. We won’t violate that because we have been just hovering around those 15,000 levels. Do you think that is a bottom or you would be surprised if that turns out to be a bottom?

A: We need a confirmation from companies on how much they have lost on their balance sheet and off- balance sheet trades. Until, companies come and tell us that the markets will speculate and will be nervous. That’s what the condition we are in right now.

Q: Can that end at the end of this quarter, if all disclosures are made?

A: I am actually skeptical that we will get all disclosures this quarter. I hope they come.

Q: Despite ICAI?

A: Yes, despite ICAI. We may not get it because ICAI does leave a room for you to disclose it in your notes. The notes will not be revealed until the balance sheets come out and that will happen only in August-September or June. It may actually go beyond this quarter. I hope that companies disclose it because if they disclose it the pain will be behind us and we will establish a bottom.

Second, we need commodity prices to come off and some dollar strength because of our inflation problem is not our problem. This time around it is actually the world’s problem and we are just importing that problem. It is going to be very hard to generate a response to that. So, we just plainly need commodity prices to come off. We need oil, wheat, and metal prices to come off.

Third, we need a little bit of despondency among retail investors. We have not seen that as yet. Retail investors are holding fort. It is quite remarkable that the market has come off as much as it has and mutual fund flows are still positive. If I get a month or two of negative mutual fund flows, I will feel a lot more comfortable that we have hit a market bottom.

Q: Do you think that the final capitulation hasn’t happened yet?

A: I don’t think so. That’s why I don’t think that the bottom that we have seen in the last couple of weeks cannot be violated. It can be violated and we could see some more downside before we bottom out. It has to be combined with these three things. I would add one more factor to this which is not an event related thing, but it is an adjustment process in the market and that’s valuation dispersion. If you look at the market even after what has happened, there are three or four sectors that are trading way above historical averages in terms of valuations and way below the gap which was much wider in January.

The three sectors on the higher side are financials, industrials, and utilities, while those that are trading at a discount are notably consumer staples, technology, and healthcare. The gap has narrowed because financials, industrials and utilities have sold off whereas staples, technology, and healthcare are relatively better but it is still there. If that gap narrows further — so if financials, utilities and industrials compress, and staples like technology and healthcare stay put — then we may also get that adjustment process required to establish a bottom.

Q: What about emerging markets overall because our rally was in sync with emerging markets and we have all underperformed the US big time this year? Do you see that continuing for the rest of the year? The US actually does not fall too much but emerging markets correct even more?

A: On the emerging market front, India and China were behaving a bit more differently from the rest of the emerging world in terms of valuations and performance. By early January, we were outperforming emerging markets by 30% from our August 2007 lows. So, we were significantly better off. Since then we have given up all the gains. Now, we are trading flat from August 2007, so that’s good news actually. That performance gap was a worry for me. We have given that up, at least relative to emerging markets. Now, we look better. Valuations were at a 100% premium on the January 9-10 peak, and are now down to 50%. I feel very comfortable with that

Q: Will that unwind more you think?

A: It could unwind more because we have domestic risk factors to deal with. So, may be it unwinds to 35%. If it goes to 35%, India becomes a very good buy relative to emerging markets.

Right now, it is neutral. It was a sell relative to emerging markets in January. It is now neutral. If it falls a bit more now — another 10-15% relative to emerging markets — we become a buy. From an emerging market standpoint, commodity prices falling, which is good for us, is actually bad for emerging markets because a lot of emerging markets are anchored around commodities. So, Brazil, Russia, West Asia, and even parts of Eastern Europe will suffer. India actually stands to gain, so if commodity prices fall and if that becomes a trigger, the country will actually outperform. That could be a major differentiating factor going forward.

Q: If we just take out the off balance sheet items like derivatives etc, do you see chances of negative surprises in core earnings over the next three quarters?

A: There is risk because EBITDA margins are actually at an all-time high. They are sitting at five-year high levels and revenue growth will slowdown because GDP growth is slowing down. I don’t think we can runaway from the fact that the economy is slowing down, which is the right response or which was the response that we should have expected when the RBI tightened last year.

This is just a reflection of what has happened last year in terms of tightening and a reflection of the slowdown in capital flows. The economy is slowing down, revenue growth therefore has to slowdown, and so earnings will slowdown. The consensus is a tad too optimistic about earnings right now. We may actually end up getting lesser earnings growth that what is being forecasted by the street which is around the 20% mark. Earnings could probably slip into the low teens or even the high single-digits. It is quite possible that if things turn really bad and some of those worst-case scenarios turn up, you get actually a quarter or two of negative earnings growth which is definitely not out there.

Q: We could de-rate further then?

A: It is possible. We are trading at about 15 times on an absolute basis, and 50% premium to the emerging market multiple. Historically, we have traded at close to the emerging market multiples, so if things turn bad one could get a bit of de-rating for a short time. If such things happen, then you would have sold your house and buy equities. Then, you satisfy the condition to really buy equities in a big way.

Q: Just one more point on sentiment. You spoke about retail not having had that capitulation yet but when you measure global and local sentiment, do you think there is more downside or do you think we are pretty much at the lowest ebb of sentiment?

A: We have a proprietary sentiment indicator where we combine 15 market matrix. A lot of them are suggesting that we are in fear zone. That’s good news. I like that because fear is essential ingredient to market bottoming out.

So, I am not getting granular about this. Normally, I don’t because I just take the composite reading and say okay, this is fear, euphoria. Now, I am getting more granular because we want to get more accurate about this. Then, there are a few indicators that are still not sold off enough or still not fallen enough. If they would fall more then we would have entrenched ourselves into a fear zone. So, from a sentiment perspective we would have probably kissed a market bottom.

Q: What’s your best case in terms of the turnaround timing? If I put a gun to your head and say by when you think the turnaround will happen, given the three factors that you mentioned where would it be — third quarter, fourth quarter, or next year? What is the highest probability of the inflation point?

A: May be by third quarter, we should have a lot of these things behind us. We will know by the third quarter whether commodity prices are going to fall or not and by that time the adjustment processes should have happened in the commodity markets. By then, we will know the losses that are there on balance sheets and the earnings slowdown that’s coming and consensus would have revised earnings lower. I am quite certain that by then retail would have given up as well, if the markets don’t go anywhere.

So, we would have satisfied a lot of these things. By the third quarter of this year, we should be okay. Therefore, long-term investors, and there are very few left these days in this market, who have a 1-2 years timeframe should actually start looking for stocks. This is a good time for them to start bargain hunting and there are a lot of places in the marketplace where things have turned attractive.

Q: Has it come as a bit of a surprise that in the last one-month, despite a fall of 30% on the index, a lot of the supposedly long-term money did not buy this dip, because at 21,000 there were a lot of India bulls? Some things have changed fundamentally but a 30% fall did not induce a whole lot of long-term money coming in?

A: It is also surprised me that institutional money has not sold heavily either and the markets have fallen 30%. We have not seen that type of selling, which if I go back to January and somebody had asked me what is going to trigger a market fall, and I would say that would be basically institutional selling. That never really came in a big way. May be we should be surprised because a lot of long-term investors were very bullish on India in 2007 and suddenly that bullishness has been threatened by a few events.

There isn’t that many really long-term investors left out there who have the luxury of taking a one-two year call. Most investors are by the mandates, which they have, forced to look at a one-three month scenario. The one-three month scenario still doesn’t look that comfortable for them to actually pull the trigger. Even the investors who are buying in this market are buying in very small quantities because they don’t want to commit their capital up front. They are saying let us put 5-10% today, and we will wait for another two-three weeks, see where prices go and put another 10%. Even the buying is happening in a very spaced out fashion. So, that doesn’t allow the market to actually bottom out.

Q: What is your base-case scenario because third quarter is the end of the pain and downside is what 10-15% from here at best?

A: I would be comfortable with 13,500 or so on the index which is the August 2007 low. We will test that. If one looks technically, the market has very strong support at 12,500. So, I am not thinking about that being broken at this stage. For that to be broken, we need really terrible news. Probably, we won’t break that but from current levels to 13,700 or 14,600 could get violated.

Q: Somewhere around July-August you think is the end of the pain?

A: Yes, third quarter is a reasonable timeframe.

Eight mistakes to avoid while investing

Eight mistakes to avoid while investing

26 Mar, 2008, 0358 hrs IST,Dhruv Agarwala & Kartik Varma,

Investing is not just about picking winners, but also about avoiding mistakes. Retail investors can be better off if they avoid making the following mistakes.

Overconfidence – Don’t be unrealistically optimistic

A bull market makes retail investors believe that they are geniuses – after all, anything they put money into goes up. This overconfidence in their own abilities leads to a complete disregard of the risks involved. Every new generation that invests in the market ignores past experience. These new investors wrongly believe that stock prices only go up.

Don’t be overconfident and don’t start believing that you have superior skills compared to the market. Recognise that in a bull market you are benefiting because the whole market is going up. If those around you are getting unrealistically optimistic, start managing your risk accordingly. Remember that sometimes markets do come crashing down.

Over enthusiasm to trade – Not every ball should be hit

Good batsmen realise that some balls outside the off-stump should be left alone. Similarly, professional investors realise that sometimes its better to just stand still than to rush into a stock. Retail investors often make the mistake of “flashing outside the off-stump” because they cannot resist the temptation to trade in every opportunity. And, like an inexperienced batsman, they suffer the same fate.

Too much trading will lead to a lot of churn, extra commissions to your broker and huge tax implications for you. Some of the world’s best investors follow a buy and hold strategy – you should too.

Missing the benefits of compounding of capital – Learn from Einstein

Albert Einstein is reputed to have said that compounding of capital is the 8th wonder of the world because it allows for the systematic accumulation of wealth. Even though any one in class 5 could tell you how compounding works, retail investors ignore this basic concept.

Compounding of capital can benefit you only if you leave your money uninterrupted for a long period of time. The sooner you start investing, the bigger the pool of capital you will end up with for your middle-aged and retirement years.

Don’t wait to start investing only when you have a large amount of money to put to work. Start early, even if it’s with a small amount. Watch this grow to a very large amount with the passage of time.

Worrying about the market – But there is no answer to your favourite question

Smart investors don’t worry about the direction of the market – they worry about the business prospects of the companies whose stocks they own. Retail investors are obsessed with the question “Where do you think the market will go?” This is a wrong question to ask. In fact, no one knows the answer.

The right question to ask is whether the company, whose stock you are buying, is going to be a much bigger business 10 years from now or not? Don’t take a view on the market, take a view on long-term industry trends and how your chosen companies can create value by exploiting these trends.

Timing the market – Around 99% of investors will fail in this strategy

Its very difficult to time the market, i.e, be smart enough to buy at the absolute bottom and sell at the absolute top. Professionals understand that timing the market is a wasted exercise.

Retail investors always wait for that elusive best opportunity to get in or to get out. But by waiting they let great investment opportunities go by. You should use systematic or regular investment plans to make investments. You’ll have to make fewer decisions and yet can accumulate substantial wealth over time.

Selling in times of panic – You should be doing the opposite

The best opportunity to buy is when the markets are falling and there is fear in the minds of investors. Yet, many retail investors do exactly the opposite. They sell when the markets are falling and buy only when the markets are high. This way they end up losing twice – by selling low and buying high, when they should be doing exactly the opposite.

If nothing has changed about the long-term outlook for the company that you own, then you should not sell this company’s stock. Use this opportunity to buy more of the same stock in falling markets. Some of the world’s biggest fortunes were made by buying when others were selling in panic.

Focusing on past performance – Its like driving forward while looking backwards

It is a very common perception that because a stock has done well in the past one year, it’s the best stock to invest in. Retail investors do not realise that often the best performers will underperform the market in the future because their optimistic outlook has already been priced into the stock.

Don’t go after hot sectors that are currently producing high returns. Don’t let greed drive your investment decisions. Look forward to see whether the gains produced in the past can get repeated or not. Short-term trends of the past might not get repeated in the future.

Diversifying too much will kill you – Investing is all about staying alive

Beyond a point, having too many names in a portfolio can be counterproductive. You might end up duplicating, or end up taking too much exposure to a sector. Over-diversification can upset your portfolio, especially when you have not done enough research on all the companies you have invested in.

If you are an active investor in the stock market, maintain a manageable portfolio of 15-25 names. Instead of adding new names to this portfolio, recognise ideal ones. Then back them with more capital. In the long-run, this will produce better returns for you than adding another 20 names to your portfolio. Investing is all is about patience and discipline. By avoiding mistakes you can improve the long-term performance of your portfolio, whatever the economic conditions prevailing in the market.

Courtesy: http://www.iTrust.in / The Economic Times

Think before you swipe credit card for cash

Think before you swipe credit card for cash

Vidyalaxmi, TNN

What’s the worst thing to do with your credit card? Use it to withdraw cash from the ATM, says a financial expert. In your monthly credit card statement, there is a mention of cash limit. That is the extent to which one could withdraw cash using a credit card. But the googly is the interest rates. It’s actually a very expensive proposition to withdraw cash as the interest rates on such withdrawals fall in the range of 40% on an annual basis.

Usually, the credit card company mentions the interest rate as a percentage per month which typically varies from 2.7-2.85% per month. And since this interest is compounded monthly, the effective annual rate of interest tends to be anywhere from 38 to 40% per annum.

Essentially, credit card companies charge the same interest rates for cash withdrawals made through credit cards and for rolling over credit card balances. But if one pays the entire amount on due date, one gets around 30-45 days of interest free credit. But what is important to know is that rule doesn’t apply in case of cash withdrawals; the credit card company levies the interest rate the moment you withdraw the cash.

Cash withdrawals can also attract an additional withdrawal fee. This charge falls in the range of 3-3.5% of the withdrawn amount. That will be added along with the interest rate to your bill. Therefore, unless you have emergency needs, do not withdraw cash on your credit card. The better option though is to go for a personal loan.

Says RL Prasad, general manager and head of cards and personal loans at Standard Chartered Bank, “You should look at this option as the last resort. If it’s a planned expenditure and you don’t have sufficient liquidity then a personal loan is be a viable option.”

Credit card cash withdrawals vs personal loan

Personal loan is a better option as the average interest rate on personal loans is between 15-20% per annum. The only handicap however, is that it takes around 7-10 working days for the banks to process personal loans.

For the uninitiated, every credit card statement has a billing date. For example, if your credit card payment is due on March 15 then the bill would have been dated around February 27.

So if you purchase anything on February 28 or later, that payment would be due only on April 15. So you get some time to cough up that money to pay off the dues. If you are unable to pay the outstanding amount, then the credit card company charges a month rate of 2.95% of the total amount. But this breather doesn’t exist on these cash withdrawals.

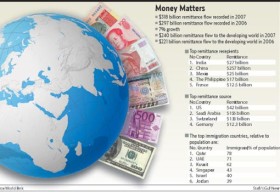

Global remittances rise 7% to Dh1.17tr

Global remittances rise 7% to Dh1.17tr

By Saifur Rahman, Business Editor Published: March 31, 2008, 00:09

Dubai: Global remittances rose seven per cent last year to $318 billion (Dh1.17 trillion) up from the previous year’s $297 billion, according to the latest World Bank report.

India topped the global list of the remittance recipients with $27 billion (Dh99.1 billion), followed by China with $25.7 billion (Dh94.32 billion), Mexico having received $25 billion (Dh91.75 billion), the Philippines $17 billion (Dh62.39 billion) and France with $12.5 billion (Dh45.88 billion).

Rich countries are the main source of remittances led by the US with $42 billion in recorded outward flows in 2006. Saudi Arabia ranks as the second largest with $15.6 billion.

Of the $318 billion, about $240 billion (Dh880.8 billion) went to developing countries last year, which is eight per cent higher than the $221 billion (811.07 billion) recorded in 2006.

These flows do not include informal channels, which would significantly enlarge the volume of remittances if they were recorded.

“In many developing countries, remittances provide a lifeline for the poor,” said Dilip Ratha, World Bank’s senior economist, and author of the report.

“They are often an essential source of foreign exchange and a stabilising force for the economy in turbulent times.”

Despite a near stagnation in remittance flows to Mexico and a deceleration in other Latin American countries contributed to a slowdown in the rate of growth of remittances, its flow to developing countries remains robust because of strong growth in Europe and Asia.

As money transfers are being subjected to more intense scrutiny by regulators, the remittance industry has experienced a shift in remittances from informal to formal channels, the report says.

But the same regulations have also increased the documentation requirements for opening bank accounts. Large money transfer operators have therefore benefited from the shifting flows.

More recently, the remittance industry has also seen the introduction of cellphone-based remittances and several pilots involving remittance-linked financial products.

Mobile banking and partnerships with cellphone companies can potentially extend remittance services to millions of people in remote, rural areas. UAE’s largest telecom operator etisalat has started a pilot project to facilitate remittances through mobile phone.

These changes may imply a shift from cash-based remittances to account-based remittances in future.

“The remittance industry is experiencing some positive structural changes with the advent of cell phone and internet-based remittance instruments. The diffusion of these changes, however, is slowed by a lack of clarity on key regulations (including those relating to money laundering and other financial crimes),” the report said.

“Remittance costs have fallen, but not far enough, especially in the South-South corridors.”

Countries in South Asia and East Asia are experiencing robust growth in remittances. In the Philippines, remittances rose by 15 per cent year-on-year during the first nine months of 2007. Both Bangladesh and Pakistan reported over 20 per cent growth in remittances during the first nine months of 2007.

“High oil prices and strong economies in the oil-exporting Middle Eastern countries are contributing to strong demand for migrant labour. In India, the largest remittance-recipient developing country, private current transfers grew by 30 per cent in the first half of 2007,” he said.

While South-South migration nearly equals South-North migration, rich countries are still the main remittances source, led by the US, according to the World Bank’s new Mig-ration and Remittances Factbook 2008, released recently.

The US was also the top immigration country in 2005, with 38.4 million immigrants, followed by the Russian Federation 12.1 million.

Among low-income countries, India had the highest immigration volume with 5.7 million, followed by Pakistan with 3.3 million.

The top immigration countries, relative to population are Qatar with 78 per cent followed by the UAE with 71 per cent, Kuwait having 62 per cent, Singapore 43 per cent, Israel 40 per cent and Jordan 39 per cent.

In many developing countries, remittances provide a lifeline for the poor.”

Dilip Ratha

World Bank’s senior economist

A time to balance

A time to balance

Manu Kaushik / Business Today March 17, 2008

Has the volatility of the past two months altered your risk tolerance level? Has the value of your stock portfolio declined alarmingly and been overtaken by bond assets, which have increased in size? In either case, your asset allocation needs a makeover.

The main challenge investors face is to earn a reasonable return while managing risk appetite. And maintaining your risk appetite means rebalancing your portfolio towards the desired asset allocation.

As things stand today, should you choose more of debt or equity? That depends on your risk tolerance levels. Market conditions have changed in the past few weeks.

But a good asset allocation strategy can help you make prudent investing decisions. “The first step towards rebalancing your portfolio is to review what you expect by way of returns and weigh that against your tolerance for risk. The state of markets (equity and debt) also decide where you ivest and how much,” says Prateek Agarwal, VP & Head (Equities), Bharti AXA Investment Managers.

Balancing it right

Keeping a diverse portfolio means among different classes of assets (e.g., stocks, debt and liquid assets) so that they work together to build your wealth, while affording you some protection from downturns in any specific asset class. Says Arpit Agrawal, MD & Group CEO, Dawnay Day AV Financial Services: “Any asset class is impacted by three basic things— momentum, liquidity and fundamentals. In the short term, momentum and liquidity play a major role, but over the long term, fundamentals are more important.”

In times of volatility, especially when the markets are shrinking, savvy investors who stick to their asset allocation make the best of a disciplined approach.

During boom times, these investors book partial profits and add on debt, and during bad times in the equity market, they sell debt and add on equities to maintain the asset allocation equilibrium. “The idea behind this rule is to keep your asset allocation within the desired risk profile. During booming markets, most investors are tempted to add more to equities, rather than book gradual profits, leading to an asset allocation mismatch. This rule brings a greater sense of discipline for an investor and provides much needed guidelines for resisting greed and temptation in rising markets,” adds Ambareesh Baliga, VP, Karvy Stock Broking.

On the other hand, when the markets are booming, adding debt by sticking to your original asset allocation can reduce the volatility. Says Sanjay Matai, Promoter, Wealtharchitects.in: “Debt funds can help you counter volatility in the markets and provide a certain degree of stability to your holdings.”

When and why

Knowing how to rebalance your portfolio is half the battle; knowing when to rebalance is the other. One way to rebalance is to increase your investment in asset categories that have fallen below your original allocation percentages. Another is to sell assets in one category and use that money to increase your investment in categories that have become underweight. Says Agarwal: “I recommend that you take a look at your portfolio at least once a year and think about pruning any asset class that has moved beyond its target by more than 5 per cent.”

Let us assume that an investor buys units in various equity funds for Rs 7 lakh, and invests Rs 3 lakh in debt funds. The objective is to maintain a constant asset mix of 70-30 through the investment horizon. The problem starts when stock and bond prices change. The reason is that movements in these asset prices will change the net asset value of the funds, and that, in turn, will change the investor’s desired mix. If the equity portion of the portfolio, for instance, increases from Rs 7 lakh to Rs 8.5 lakh, while the bond portion moves to Rs 1.5 lakh, the total equity exposure will be 85 per cent. This is clearly in excess of the investor’s desired equity exposure. Under such circumstances, the investor must cut equity in the portfolio by Rs 1.5 lakh to maintain the ideal mix.

Once you get started, it’s not a difficult thing to follow. But the best part is that you will, by default, add equity to your portfolio when the times are bad and, thus, buy stocks at cheap prices, and book profits when the times are good.

Eight mistakes to avoid while investing

Eight mistakes to avoid while investing

26 Mar, 2008, 0358 hrs IST,Dhruv Agarwala & Kartik Varma,

Investing is not just about picking winners, but also about avoiding mistakes. Retail investors can be better off if they avoid making the following mistakes.

Overconfidence – Don’t be unrealistically optimistic

A bull market makes retail investors believe that they are geniuses – after all, anything they put money into goes up. This overconfidence in their own abilities leads to a complete disregard of the risks involved. Every new generation that invests in the market ignores past experience. These new investors wrongly believe that stock prices only go up.

Don’t be overconfident and don’t start believing that you have superior skills compared to the market. Recognise that in a bull market you are benefiting because the whole market is going up. If those around you are getting unrealistically optimistic, start managing your risk accordingly. Remember that sometimes markets do come crashing down.

Over enthusiasm to trade – Not every ball should be hit

Good batsmen realise that some balls outside the off-stump should be left alone. Similarly, professional investors realise that sometimes its better to just stand still than to rush into a stock. Retail investors often make the mistake of “flashing outside the off-stump” because they cannot resist the temptation to trade in every opportunity. And, like an inexperienced batsman, they suffer the same fate.

Too much trading will lead to a lot of churn, extra commissions to your broker and huge tax implications for you. Some of the world’s best investors follow a buy and hold strategy – you should too.

Missing the benefits of compounding of capital – Learn from Einstein

Albert Einstein is reputed to have said that compounding of capital is the 8th wonder of the world because it allows for the systematic accumulation of wealth. Even though any one in class 5 could tell you how compounding works, retail investors ignore this basic concept.

Compounding of capital can benefit you only if you leave your money uninterrupted for a long period of time. The sooner you start investing, the bigger the pool of capital you will end up with for your middle-aged and retirement years.

Don’t wait to start investing only when you have a large amount of money to put to work. Start early, even if it’s with a small amount. Watch this grow to a very large amount with the passage of time.

Worrying about the market – But there is no answer to your favourite question

Smart investors don’t worry about the direction of the market – they worry about the business prospects of the companies whose stocks they own. Retail investors are obsessed with the question “Where do you think the market will go?” This is a wrong question to ask. In fact, no one knows the answer.

The right question to ask is whether the company, whose stock you are buying, is going to be a much bigger business 10 years from now or not? Don’t take a view on the market, take a view on long-term industry trends and how your chosen companies can create value by exploiting these trends.

Timing the market – Around 99% of investors will fail in this strategy

Its very difficult to time the market, i.e, be smart enough to buy at the absolute bottom and sell at the absolute top. Professionals understand that timing the market is a wasted exercise.

Retail investors always wait for that elusive best opportunity to get in or to get out. But by waiting they let great investment opportunities go by. You should use systematic or regular investment plans to make investments. You’ll have to make fewer decisions and yet can accumulate substantial wealth over time.

Selling in times of panic – You should be doing the opposite

The best opportunity to buy is when the markets are falling and there is fear in the minds of investors. Yet, many retail investors do exactly the opposite. They sell when the markets are falling and buy only when the markets are high. This way they end up losing twice – by selling low and buying high, when they should be doing exactly the opposite.

If nothing has changed about the long-term outlook for the company that you own, then you should not sell this company’s stock. Use this opportunity to buy more of the same stock in falling markets. Some of the world’s biggest fortunes were made by buying when others were selling in panic.

Focusing on past performance – Its like driving forward while looking backwards

It is a very common perception that because a stock has done well in the past one year, it’s the best stock to invest in. Retail investors do not realise that often the best performers will underperform the market in the future because their optimistic outlook has already been priced into the stock.

Don’t go after hot sectors that are currently producing high returns. Don’t let greed drive your investment decisions. Look forward to see whether the gains produced in the past can get repeated or not. Short-term trends of the past might not get repeated in the future.

Diversifying too much will kill you – Investing is all about staying alive

Beyond a point, having too many names in a portfolio can be counterproductive. You might end up duplicating, or end up taking too much exposure to a sector. Over-diversification can upset your portfolio, especially when you have not done enough research on all the companies you have invested in.

If you are an active investor in the stock market, maintain a manageable portfolio of 15-25 names. Instead of adding new names to this portfolio, recognise ideal ones. Then back them with more capital. In the long-run, this will produce better returns for you than adding another 20 names to your portfolio. Investing is all is about patience and discipline. By avoiding mistakes you can improve the long-term performance of your portfolio, whatever the economic conditions prevailing in the market.

Courtesy: http://www.iTrust.in / The Economic Times

Tips for small retail investors to ease their nightmares

Tips for small retail investors to ease their nightmares

17 Mar, 2008, 1620 hrs IST,Shakti Shankar Patra, TNN

Ranjit Sehgal works as a system analyst at one of the top IT companies of India. Apart from forwarding emails, which his job requires him to do, he passionately tracks the domestic equity market. His favourite anecdote about the market until recently was: “Each time the market crashes, if you sell your house and invest in the stock market, in a month, you’ll be able to move a couple of suburbs closer to South Mumbai.”

Two months ago, all you had to do was name a stock and he would have told you its last traded price. You name a brokerage and he would have told you which stocks they were betting on. Any news or rumour, no matter how trivial, as long as it was remotely related to the equity market, he had it covered.

A day didn’t pass by without him arguing, disputing, advising or seeking advice on various message boards on the internet. He was a much sought-after man by friends and acquaintances, who had all heard of his uncanny ability to spot a multi-bagger and wanted to find a better avenue for their cash than the low-risk low-return bank deposit. He followed his own advice and put all the money he had to spare into stocks — for he believed that stocks were king.

But that was then. Today, with the Sensex in a free fall and bears mauling virtually every stock, Ranjit is in a funk. He has not logged on to his demat account for the past couple of days and zaps the business channel the moment it comes on.

His portfolio has lost over half its value and every passing day seems to erode it further. Ditto with the message boards, which are now filled with jokes like: ‘the easiest way to make a million through the stock market is to start with two million’.

He just can’t understand what went wrong. During the past three years, each time the market had corrected sharply, he had bought into it and turned in a heavy profit. He had done his own analysis, mapping the Sensex against the Dow and had been convinced that decoupling was taking place.

This time round, too, he had bought into the Sensex when it first fell in January and sure enough, it had rebounded. Then, when it fell again he bought even more. Unfortunately, it has never recovered since and he suddenly finds himself sitting on a mountain of useless paper.

Most investors are likely to identify with Ranjit’s predicament. Suddenly, that demat account is a nightmare and the fixed deposit a dream investment. While there may be many who are undergoing this traumatic experience for the first time, old market hands will tell you that this is just an umpteenth rerun of greed melting into fear.

The real predicament that they now face is: Where does one go from here? While there is no one-size-fits-all solution, here is some advice that small retail investors can use to mitigate the nightmares they are enduring…

Never hold on to what you won’t buy now

There’s no point in burying your head in the sand like an ostrich and waiting for a miraculous rebound. An active interest in the state of affairs is a must. The first thing you should do is take a long, hard look at your portfolio.

Does it have more of established companies with proven track records, or does it consist more of stocks like Nagarjuna Fertilizers & Chemicals and Reliance Natural Resources (RNRL), which you bought because they were ‘momentum plays?’

Having done that, get rid of the momentum stocks. After all, with the momentum gone, it’s time for these stocks to go as well. The rule is simple: ‘Never hold on to something that you wouldn’t buy now’ . Never ‘hope’ or ‘pray’ . It is either a ‘buy’ or a ‘sell’.

So, it doesn’t matter at what price you bought such stocks — just dump them and collect whatever cash you can. If you have blue-chips in your portfolio like Reliance Communications, Bharti Airtel, Hindustan Unilever or ICICI Bank, to name but a few, you can actually choose not to sell them. In the long run of say, 3-5 years, there is a good chance that you will still earn a return higher than what a bank deposit can give you in the same time period.

Once bitten twice shy

Having lost money in the market, it is but natural that you may have decided to stay away from it totally. That, however, is not such a smart thing to do. As any seasoned investor will tell you, the best time to buy is during a bear market. That said, it is important to keep returns expectations realistic and ensure that you get into stocks, which have a sound business model and visible cash flow. When you invest in a stock, you are basically buying a small stake in a company.

Generally, people tend to ignore this fact. But the moment you ask yourself about the company you want to own, the answer is definitely, Reliance Industries and not Nagarjuna Fertilizers; it is definitely Infosys, but certainly not Himachal Futuristic. It is important to buy stocks for their intrinsic worth and not on the basis of expected short-term gains.

Only fools rush in where angels fear to trade:

If you are someone who was sitting on the fence with cash, praying for a correction, ready to jump in for his first investment in equities, then remember to go easy. For only fools rush in where angels fear to trade. Although buying into a correction is something that has paid rich dividends in the past 3-4 years, the same may not necessarily be the case this time.

With global financial markets in turmoil and a general election looming on the horizon, you would do well not to assume that the market has bottomed out. Just because the stock you were planning to buy has fallen to 50 from 100, doesn’t mean that it cannot go to 25. So, try and enter in a staggered manner. In times such as these, as the saying goes: ‘cash is king’ .

Sense and sensex:

Often, investors get too obsessed with the level of the Sensex and forget to concentrate on the fundamentals of the stocks that they hold. There are umpteen instances of individual stocks underperforming in a bull market and those outperforming even in a bear market.

This is because the index reflects the entire market and does not necessarily reflect what is happening with your stock. So, let analysts talk about Sensex levels while you track your stock.

India, still shining:

With the garbage out of the house, we need to decide what stocks to buy, if any. Just because the decoupling theory has been thrown out of the window doesn’t mean that we are absolutely married to the US economy.

Although a slowdown in the US will affect export-oriented industries in India, it will have a limited impact on most of India Inc, since by and large, the India story is about domestic consumption, rather than exports.

And if the Budget is anything to go by, then the government is definitely in a mood to leave more money with consumers. With more money to spend, the sectors that are expected to benefit are consumer durables, FMCG and retail, to name a few.

The relative outperformance that these sectors have shown during the current turbulence is a good indicator that they may well hold their own even in a bear market. For some of ETIG’s top picks within these sectors, take a look at the stock ideas discussed in the current edition.

Money matters:

Lastly, and most importantly, the fact remains that we had an absolutely unbelievable and overtly extended bull run of around five years. During this period, the Sensex went up seven times, with most stocks going up exponentially.

This couldn’t have continued till eternity. But at the same time, this doesn’t mean the end of the world. Equity markets always swing between overexuberance and absolute despair.

So, don’t lose heart; there will be an end to this carnage. But to enjoy the fruits of the next boom, invest in fundamentally sound companies and always have a substantial amount of cash in hand. For, while you can buy a future multi-bagger today, tomorrow it may end up being a lot cheaper.

You must be logged in to post a comment.