Month: December 2007

Be wise in what you ask for

Be wise in what you ask for

29 Dec, 2007, 0003 hrs IST,Vithal C Nadkarni, TNN

On New Year, be careful of what you ask. You might actually get it! That warning has been variously attributed to Vyasa and Valmiki. In the Mahabharata, for instance, Vyasa narrates an intriguing ‘explanation’ behind Draupadi’s becoming a common wife to the five Pandava princes. She’s supposed to have propitiated Siva with her austerities in her previous incarnation. When the blue-throated Lord asks his devotee to choose a boon, she begs for a groom with all the great qualities.

Not being content to voice her request once, the pushy girl goes on to repeat her wish five times. “So be it,” says the Lord. “Since you spoke five times, five husbands you shall have, but in your next life.” Now why didn’t the Lord grant her wish immediately? Perhaps he wanted to spare his devotee the agonies of the Great War, which was certain to occur once his heroic bratpack made its bid for kingly spoils from older, entrenched bloodlines. Nor does Siva excuse his devotee’s excess in the story as narrated by Vyasa. His motto seems to be, “You have only to ask and you shall have it.”

This is not unlike what the Australian TV-producer Rhonda Byrne has articulated in her best-selling The Secret, namely, for better or worse, you’ll get what you wish for. So, be very careful.

Valmiki’s version of the power of misplaced wishing involves Ravana and his brothers. The Danava brood wins over Brahma with their tapasya and is asked to make their wishes: Ravana asks for immunity from all the gods, anti-gods, the nagas and other semi-divine beings in the seven worlds. His attempt is to cover all the major bases from which he anticipates attack. But he neglects to include puny humans, which proves to be his nemesis. He might have been saved had he eschewed toxic thinking and chosen as his youngest sibling Vibhishana did, namely, constant proximity to the Lord and His good cause.

The mighty Khumbhakarna, too, slips in his unseemly hurry to ask for the Indrasana or sovereignty over the gods. He asks for Nidrasana instead, which involves suzerainty over inordinate sleep and inertia.

Closer to our times watch the paradox of “millions longing for immortality who do not know what to do on a rainy Sunday afternoon,” writes the novelist Susan Ertz. Just think of the prospects of living forever in a world gone to pot from pollution and perverted nature. Mere quantity isn’t enough. Think of the quality. Strive for it.

Cheer up, the outlook is not so bad

Cheer up, the outlook is not so bad

27 Dec, 2007, 0548 hrs IST,T T Ram Mohan, TNN

The year ends on a sombre note for the world economy. The impact of the subprime crisis in the US is stretching out. Whatever the prospects of an economic depression, the barrage of morose comment is certain to generate pervasive mental depression.

Cheer up, the outlook is not so bad. The US economy will slow down appreciably but still looks unlikely to go into recession, that is, two successive quarters of negative growth. The global economy too will slow down but growth will still be good by past standards. The Indian economy will continue to grow strongly and the stock market should provide attractive returns over the coming year.

The fundamental basis for optimism about the world economy is this: major economic crises have their roots in big supply shocks (e.g., a sharp rise in oil prices) or a currency crisis (caused by foreign investors’ lack of confidence in an economy) or a banking crisis. None of this appears likely today.

The world economy has shown an uncanny ability to live with high oil prices. But prices above $100 still have the potential to cause damage. During the year, prices inched towards the $100 mark but they have since shown signs of softening. A big factor is the US intelligence agencies’ assessment that Iran suspended its nuclear weapons programme in 2003 and is still quite far from acquiring the bomb. This renders a neocon-inspired strike on Iran rather difficult in the coming year. That is good news for oil prices.

The US is hugely indebted and foreigners hold a huge amount of US government securities. The US is theoretically vulnerable to a currency crisis. But currency crises are more common when debt is foreign currency-dominated. This is not true of the US.

The US enjoys an even bigger advantage. As the world’s sole superpower and the biggest economy, the US will remain the choice of central banks and other investors for some time to come. While investors may lower their US holdings in their portfolios, a big sell-off that could trigger a currency crisis is just not on the cards.

What about a banking crisis? Banks’ losses are expected to rise in the months to come as the crisis unfolds. Many of the off-balance sheet vehicles floated by banks are now coming on to their balance sheets. As banks are expected to carry a minimum of regulatory capital against balance sheet assets, it is argued that their ability to extend credit will be impaired and we could see a credit crunch.

This is true, of course, but a credit crunch does not imply a banking crisis. A banking crisis involves the failure of several banks, that is, the net worth of several banks gets wiped out. There is nothing so far to suggest that such a crisis threatens American banking. Large banks operate with a capital adequacy ratio of over 12% against the regulatory minimum of 8% or so. They are well placed to absorb the impact of the subprime crisis and also to boost their capital.

That is because, as Citibank and UBS have shown, there are overseas investors willing to provide capital.

US banks have non-core assets that could be sold off at a pinch. Secondly, as the Financial Times points out, the global US banks are sitting on a gold-mine in the form of their investments in Chinese banks — the nine biggest stakes are worth $81 billion compared to the write-offs announced of $50 billion. So, yes, banks’ ability to lend will be constrained but this falls well short of a banking crisis.

The prospects, therefore, are of a slowdown in the US economy but not a recession. A US slowdown will drag down global economic growth, of course, but strong domestic demand in emerging markets can be expected to mitigate this impact. Despite what is believed to be a crippling credit crisis, world economy growth in 2008 in PPP terms will not be much lower than the rate of 4.4% seen in 1999-2008.

India’s own growth prospects remain bright. In 2008-09, we can expect growth of the order of 8%-8.5%. Exports are bound to be impacted by external conditions and the appreciation of the rupee. But investment will remain strong.

The big change in the Indian economy in recent years is that it is becoming investment-driven: investment has outstripped consumption in its contribution to growth every year since 2002-03. Businessmen are looking far beyond the present global conditions and they like what they see in India, so they will invest and invest.

India’s stock market should continue to deliver good returns. The earnings outlook remains good. Moreover, the Indian stock market is showing signs of attracting new classes of investors (US pension funds, oil wealth, Japanese retail investors, etc). The combination of strong fundamentals and FII flows augurs well for the market.

There is an economic crisis in our midst alright. But it is not formidable in relation to crises we have seen in the past. On balance, it is still amenable to concerted policy action. Not a bad note on which to usher in the New Year.

Stocks to buy: Kotak Mahindra Bank, Titan Industries, Salora Intl, 3i Infotech, Colgate Palmolive

Stocks to buy: Kotak Mahindra Bank, Titan Industries, Salora Intl, 3i Infotech, Colgate Palmolive

28 Nov, 2007, 0719 hrs IST, TNN

Kotak Mahindra Bank

CMP: Rs 1,122.35

Target Price: Rs 1,363

Motilal Oswal Securities has initiated coverage on Kotak Mahindra Bank with a buy rating and a price target of Rs 1,363. “Kotak (Bank) is aggressively building up its banking franchise, with focus on affluent customers and retail services. Its asset management business should see exponential growth,” the Motilal Oswal note to clients said.

“Though its insurance business has been losing market share, we expect better utilisation of Kotak’s distribution strength to change this. We believe KMB deserves premium valuations, given the strong growth expected across its businesses, fast traction in earnings, and quality management,” the note added.

Titan Industries

CMP: Rs 1,531.70

Target Price: Rs 1,850

Merrill Lynch has initiated coverage on Titan Industries with a buy rating and a price target of

Rs 1,850, terming it a “high growth domestic consumption story.” “We expect Titan’s watch business to benefit from mix up-trading and distribution moving more towards high margin channel of ‘World of Titan’”.

“In jewellery, we expect volume growth to remain explosive at around 40% as Titan forays into second-tier cities with the new value format “Gold Plus”,” the Merrill note to clients said. “In the premium “Tanishq” format, larger stores and higher efficiencies should drive margins. Lastly, we expect the new venture of prescription eyewear to take off and account for 4% of EBITDA (earning before interest, taxes, depreciation and amortisation) FY10,” the note added.

Salora Intl

CMP: Rs 223

Target Price: Rs 312

Parag Parikh Financial Advisory Services has assigned a buy rating to Salora International with a price target of Rs 312. “The company derives 85% of its revenues from the telecom & infocom distribution business and more than 90% of the EBIT (earnings before interest and taxes) from the business of distribution, thus making it a clear contender for a re-rating from a CTV components manufacturer to a full-fledged distributor,” the PPFAS note to clients said.

“The company has active plans to get into retailing of products that it is already distributing; the modalities of the same will be out very shortly. The company is very well placed to show a topline growth of above 35% for some time in our expectations,” the note further said, adding that the recently initiated restructuring of the CTV components business will keep overall profitability intact.

3i Infotech

CMP: Rs 134.60

Target Price: Rs 175

ICICI Securities (I-Sec) has initiated coverage on 3i Infotech with a buy rating and a price target of Rs 175. “3i Infotech, with a balanced mix of software products and services (~1:1), has differentiated itself from peers by adopting a diversified business model with a strong foothold in high-growth areas.

With software services providing stability to revenue stream, products add non-linearity to the overall business model,” the I-Sec note to clients said. Additionally, the sharp rupee appreciation, which has baffled the whole software sector, is relatively a lesser concern for 3i Infotech as it derives around 31% revenues from the domestic market and the net dollar exposure is estimated to be less than 10%. Also, 3i Infotech remains comparatively aloof from other sectoral worries such as the subprime issue, impending economic slowdown in the US, wage inflation, attrition,” the note added.

Colgate Palmolive

CMP: Rs 410.35

Target Price: Rs 482

Citigroup Global Markets has assigned a buy rating to Colgate Palmolive with a price target of Rs 482. “Colgate’s business has demonstrated strong growth over the eight quarters, with sales growing in excess of 15%. It has gained share in rural areas through its ‘Cibaca’ brand and has also rolled out innovative toothpaste variants at the higher end, which have gained strong acceptance and helped accelerate growth,” the Citigroup note to clients said.

“With major capital expenditure behind it, and incremental tax and excise savings from its new plants, cash generation is likely to accelerate. We estimate about Rs 1,230 crore of free cash generation over the next three years, more than two times of what was generated over the previous three years and as such, dividend payout could increase,” the note added.

Disclaimer: The above stocks are picked up at random from research reports of brokerage houses. Investors are advised to use their own judgement before acting on these recommendations. ET does not associate itself with the choices.

OVL hits oil in Najwat block off Qatar shores

OVL hits oil in Najwat block off Qatar shores

28 Dec, 2007, 0448 hrs IST,Rajeev Jayaswal, TNN

NEW DELHI: ONGC Videsh Ltd (OVL) has struck black gold in Arabian Gulf block off Qatar. The Najwat Najem block is the first overseas project executed by OVL wherein the company has both 100% ownership and is the sole operator.

“As per preliminary indications, oil has been encountered in the Shuaiba and Arab formations. The second well will also be completed by January 2008. We are hopeful that this will lead to the development stage,” a source in the petroleum ministry said.

The exact size of the discovery is not known yet as it has not been formally approved. OVL spudded its first appraisal well in the Najwat Najem structure on July 6, 2007. OVL had firmed up two locations for evaluating the structure and assessing and proving its commerciality.

OVL signed an appraisal, development and production sharing agreement (ADPSA) with the Qatari government on March 2, 2005 for the Najwat Najem oil structure appraisal in the country as an operator. The agreement came into effect on May 19, 2005 with the signing of the Emiree Decree (termed the effective date).

ADPSA is for a period of 20 years from the date of the Emiree Decree and comprises of an initial two year appraisal phase followed by a development phase. The minimum work committed during the appraisal phase is reprocessing and interpretation of 200 sq km of seismic data, a preliminary G&G study, drilling of two appraisal wells and an integrated multi-disciplinary study to assess the potential of the area.

The Najwat Najem oil structure is located in the Arabian Gulf in offshore Qatar at a distance of about 100 km north east of Doha Port. It lies at a distance of about 18 km off the Halul island in the state of Qatar. The Jurassic lime stones are the main reservoirs of this structure.

The Najwat Najem oil structure is in the Persian Gulf, at a water depth of approximately 135 feet.

India’s November oil product sales up 5.5 pct

India’s November oil product sales up 5.5 pct

28 Dec, 2007, 1327 hrs IST, REUTERS

NEW DELHI: India’s domestic oil product sales in November rose 5.5 percent from a year earlier to 10.6 million tonnes, official data showed on Friday. Domestic diesel sales were up 10.3 percent to 4.1 million tonnes from a year earlier, the data showed.

HPCL sells Jan stem to Emirates National Oil Co

HPCL sells Jan stem to Emirates National Oil Co

27 Dec, 2007, 1316 hrs IST, REUTERS

SINGAPORE: Hindustan Petroleum Corp Ltd (HPCL) has sold via tender 25,000-30,000 tonnes of January-loading fuel oil to Emirates National Oil Co (ENOC) at an undisclosed price, traders said on Thursday.

The 380-centistoke (cst) cargo, of 4.0 percent sulphur and 0.998 density, is for loading on Jan. 14-16 from its Vizag terminal, on a free-on-board (FOB) basis.

HPCL last sold a similar lot, for Dec. 15-17 loading from Vizag at a discount of $20-21 a tonne to Singapore spot quotes, on an FOB basis. The cargo was also picked up by ENOC and was re-sold into the Singapore marine fuel market, the world’s largest, traders said.

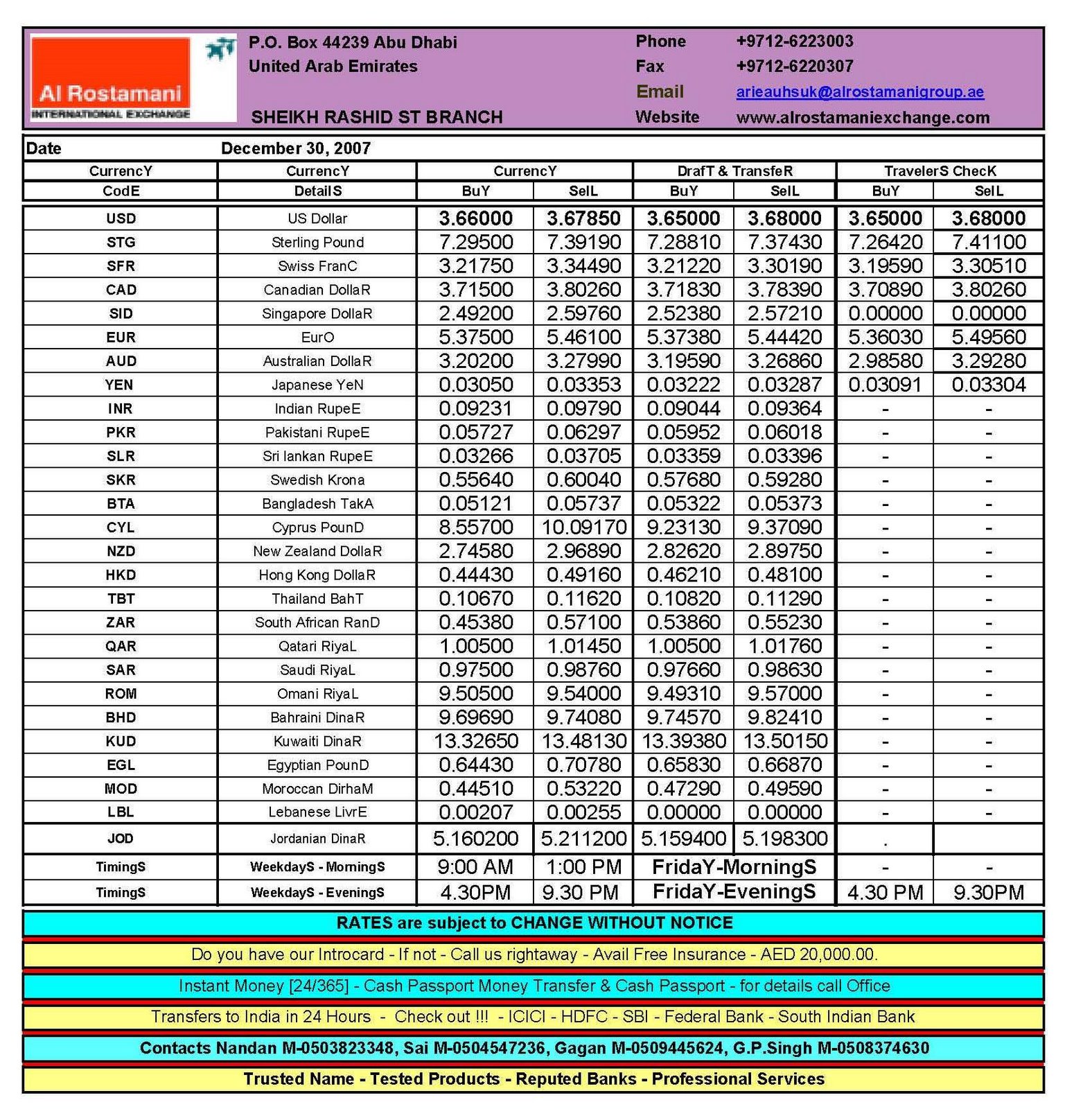

Daily Exchange Rates – Saturday, 29 December 2007

Brought to you by

Al Rostamani International Exchange

Abu Dhabi

Phone: +9712 6223003

http://www.alrostamaniexchange.com

Adnoc to supply full term crude for February

Adnoc to supply full term crude for February

Reuters GULF NEWS Published: December 28, 2007, 00:32

Tokyo: Abu Dhabi National Oil Co (Adnoc) will supply full term volumes of crude oil to its Asian customers for February, the same as January, in line with expectations, traders said yesterday.

On top of the contracted volumes, Adnoc is expected to supply additional spot barrels to some lifters upon request for a third straight month, they added.

Adnoc occasionally sells extra crude to its term buyers in Asia, its main export market, though exact volumes to be supplied were not immediately known.

Three lifters had received written notices that they would get full term volumes for a third month in February and did not ask for extra barrels. “It was exactly at the contracted levels,” one source said. “We had been thinking that there would be no cuts.”

Traders said Adnoc was likely to supply additional volumes of light sour Murban crude for February as spot cargoes to some lifters in need, but one said the volumes will be limited.

When lifters decide to take additional spot crude from Adnoc, they buy at the grade’s official selling price without having to pay a premium in the spot market. The spot differentials for middle-distillates-rich Murban crude for February loading have stayed at a premium of around 20-25 cents a barrel to Adnoc, reflecting winter demand.

A trader said Adnoc offered additional offshore Upper Zakum crude to some lifters, but it was not clear whether any lifter accepted the offer.

Amrita Super Star Caravan in Dubai – 28 December 2007

Dear all,

Excellent, enthralling, everlasting – words are not enough to express the sheer joy of watching the young dynamites as well as the Superstars perform live. And what a performance by Shivamani to end the show.

May AMMAs blessings and God’s grace be with all these talented stars to perform better and better in the coming years too.

Ramesh Menon

28122007

Movie Review – Taare Zamin Par

Movie Review – Taare Zamin Par

Every Child is Special

Dear friends,

Do not miss watching this movie. Excellent one to end 2007 Indian Hindi movies on an ever high note. Every working parent should watch this and for all those who dictate their way with their children this will be a great lesson. Congratulations to Amir Khan and the young Darsheel Safary and also to Tisca Chopra and Vipin Sharma for brilliantly living their roles throughout. Good songs and photography too.

Take all those kids and loved ones along.

Regards,

Ramesh Menon

http://www.team1dubai.blogspot.com

- ← Previous

- 1

- 2

- 3

- …

- 13

- Next →

You must be logged in to post a comment.